The IMF Looks at Budget Institutions in G-20 Countries

The International Monetary Fund recently published a study on budget institutions in G-20 countries. The study takes stock of these countries' progress in reforming their budget institutions and examines whether having strong budget institutions has helped countries tackle their budget challenges in the aftermath of the financial crisis. While it is difficult to measure the impact of institutional arrangements on budgetary outcomes, the IMF's verdict is that they do matter.

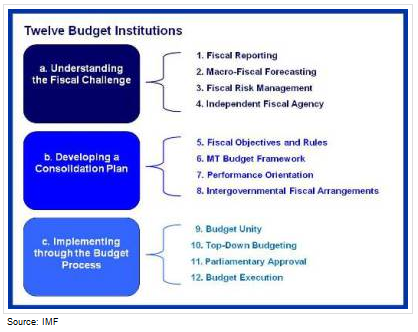

The study identified 12 institutions – including processes, systems, legal frameworks and organizational entities – that are believed to improve the effectiveness of fiscal policy. These institutions were grouped into three categories: those that help people understand a country's fiscal situation, those that help lawmakers plan appropriate and credible fiscal adjustments, and those that implement the government's budget. The IMF assessed the strength of these institutions in each G-20 country, and looked at efforts to improve these institutions since 2010.

While many G-20 countries have strengthened their budget institutions, much of the heavy lifting has occurred in Europe in response to the sovereign debt crisis. Across the G-20, most progress has been made in establishing independent fiscal councils, fiscal rules, and medium-term budget frameworks. However, less has been done to enhance fiscal transparency, including steps such as reporting balance sheet positions, fiscal risk, and intergovernmental fiscal arrangements. In addition, few countries have taken steps to strengthen implementation, for instance, by having legislative arrangements to approve the annual budget.

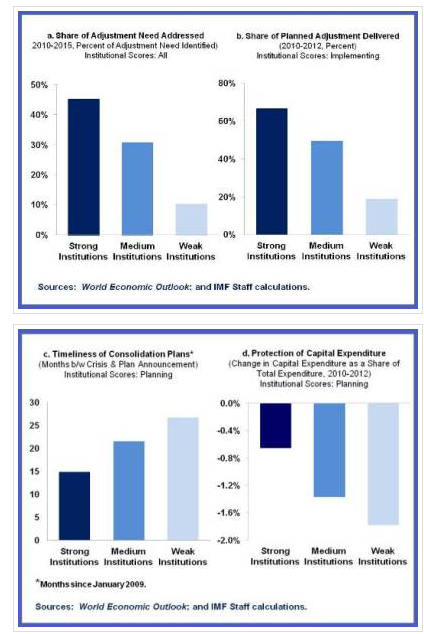

So what's the evidence that these institutions produce better fiscal outcomes? The study shows that countries with stronger budget institutions overall have addressed a greater share of their fiscal adjustment needs, and those with stronger implementation institutions generally had more success in delivering on their announced plans. Countries with stronger planning institutions were generally faster to announce strategies to strengthen public finances post-crisis and were better at protecting public investment as part of those strategies.

Of course, there are limitations to this analysis, which the IMF readily acknowledges. Not only is the period of analysis brief, but it is difficult to disentangle the relative impact of institutional factors from other determinants of fiscal policy success such as the political context and macroeconomic environment.

The IMF also provides an analysis of U.S. budget institutions as part of its detailed country evaluations. While it notes that the U.S. has recently introduced a number of fiscal rules to rein in spending – specifically the caps on discretionary spending and the reinstatement of PAYGO – it argues that their effectiveness is limited by their inability to deal with the built in growth of mandatory programs, which present some of the biggest threats to fiscal sustainability, and the exemptions in PAYGO. The IMF says the lack of medium-term fiscal goals, absence of political consensus, and fragmented budget process are all roadblocks to enacting a deficit reduction plan with a more gradual pace and more desirable composition. Its key recommendations for the U.S. include:

- Establishing medium-term spending ceilings that address both mandatory and discretionary spending

- Eliminating exemptions to PAYGO that do not serve countercyclical macroeconomic objectives

- Limiting fragmentation of the budget process through the adoption of a single comprehensive appropriation bill

- Aligning increases in the debt ceiling with the annual comprehensive budget resolution

We agree with the IMF that much can be done to strengthen U.S. budget institutions and improve the budget process. While these reforms cannot solve all of our nation's fiscal problems, they can improve our understanding of the long-term challenges and help pave the way for appropriate action. The IMF's recommendations overlap with those from the Peterson-Pew Commission, so it is encouraging to see agreement on ways we can improve the process to encourage greater fiscal responsibility.