Wrapping up the 2016 Fiscal Year

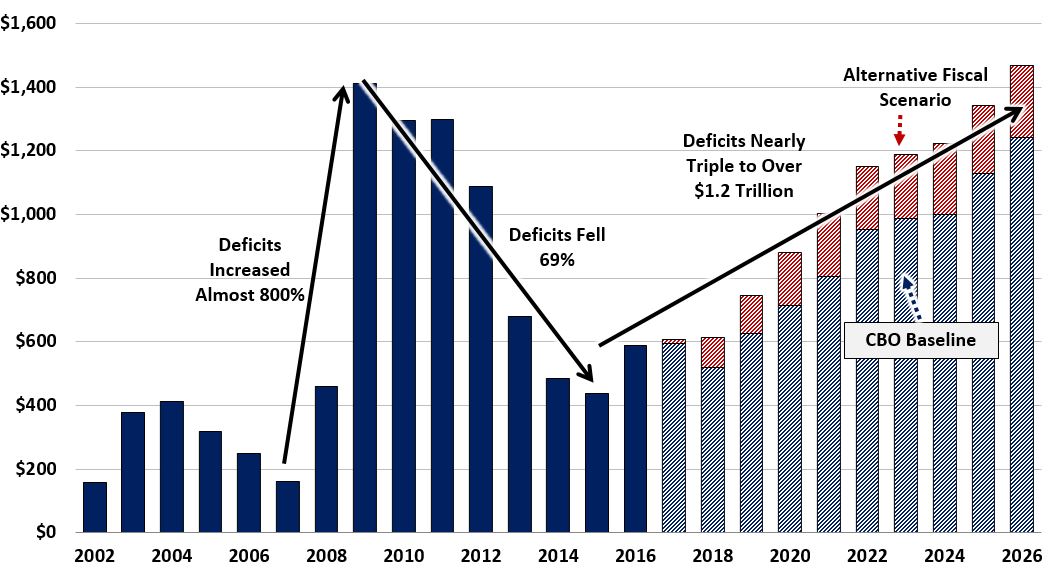

The Fiscal Year (FY) 2016 budget deficit totaled $587 billion, according to the final data from the Treasury Department. Although this is nearly 60 percent below the 2009 peak, it is 34 percent larger than last year’s $438 billion level. While this year’s deficit is not the main cause for concern about our fiscal path, it is a precursor to projected deficit increases as the debt continues on its unsustainable course.

From 2009 to 2015, the budget picture changed significantly, with deficits falling by 69 percent – from $1.4 trillion to $438 billion. This reduction was driven mainly by a large increase in tax collections that has come largely as a result of the economic recovery and expiring stimulus measures but also due to new taxes from the American Taxpayer Relief Act, the Affordable Care Act, and increased remittances from the Federal Reserve. At the same time, nominal spending was only slightly higher than in 2009.

But after last year's passage of tax extenders, an unpaid-for doc fix, and an increase in the discretionary spending caps, the 2016 deficit projection went from about stable with 2015 (projected to be $467 billion in the Congressional Budget Office's January 2015 baseline) to an increase of 34 percent. Between 2015 and 2016, revenue barely grew at all, while spending grew at a steady 4.5 percent rate.

| Annual Totals | Change from 2015-2016 | |||||

|---|---|---|---|---|---|---|

| 2007 | 2009 | 2015 | 2016 | Dollars | Percent | |

| Revenue | $2,568 | $2,105 | $3,250 | $3,267 | $17 | 0.5% |

| Individual Income Taxes | $1,163 | $915 | $1,541 | $1,546 | $5 | 0.3% |

| Payroll Taxes | $870 | $891 | $1,065 | $1,115 | $50 | 4.7% |

| Corporate Income Tax | $370 | $138 | $344 | $300 | -$44 | -12.9% |

| Other Revenue | $165 | $161 | $300 | $306 | $6 | 2.0% |

| Primary Spending | $2,492 | $3,331 | $3,465 | $3,613 | $148 | 4.3% |

| Defense | $529 | $637 | $591 | $595 | $4 | 0.7% |

| Social Security | $581 | $678 | $882 | $916 | $34 | 3.9% |

| Medicare (net) | $371 | $425 | $540 | $595 | $55 | 10.2% |

| Other Primary Spending | $1,011 | $1,591 | $1,452 | $1,507 | $55 | 3.8% |

| Interest on debt | $237 | $187 | $223 | $241 | $18 | 8.0% |

| Deficit | $161 | $1,413 | $438 | $587 | $149 | 34.0% |

Source: CBO, Treasury Department, CRFB calculations

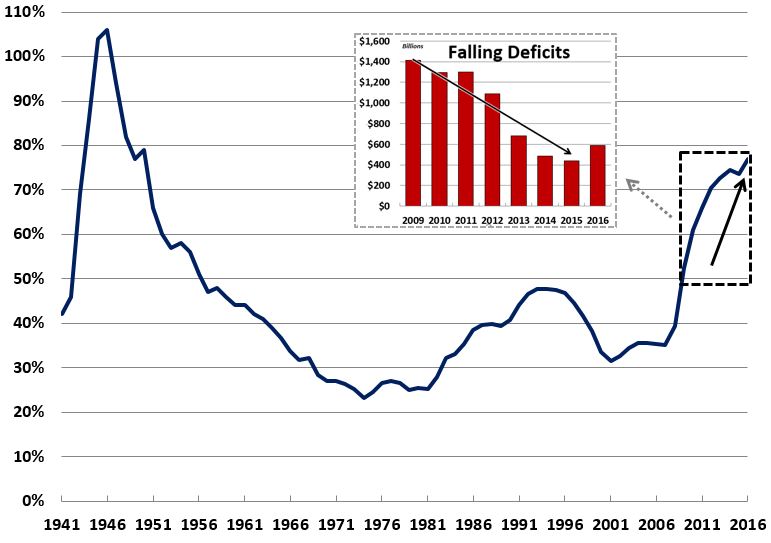

Arguably, the most important metric of a country’s fiscal health is its ratio of debt to Gross Domestic Product (GDP). And unfortunately, even as deficits fell, debt continued to grow in nominal dollars and as a share of the economy. Since 2009, deficits have fallen by 60 percent, but nominal debt held by the public has grown by about 90 percent – from $7.5 trillion to $14.2 trillion. As a percentage of GDP, debt has also grown rapidly, from 35 percent of GDP in 2007 to 52 percent in 2009 and nearly 77 percent in 2016. This puts debt at twice the 50-year historical average of 39 percent of GDP and leaves it near record-high levels not seen other than in the period around World War II.

The deficit remains over three and a half times as high as in 2007 (just over 2 percentage points higher as a percent of GDP) and is projected to grow over time. Under CBO’s current law baseline, annual deficits will return to trillion-dollar levels by 2024. Under a more pessimistic Alternative Fiscal Scenario in which policymakers fail to pay for new spending and extended tax cuts, trillion-dollar deficits return by 2021 and reach $1.5 trillion – a nominal-dollar record – by 2026.

***

Though deficits have declined in recent years, the good news has ended; the era of declining deficits is over. This year’s deficit has risen 34 percent from last year, and CBO expects trillion-dollar deficits to return by 2024. Meanwhile, debt will reach a new post-World War II era record of 76 percent of GDP at the end of 2016 and rise further to 86 percent of GDP by 2026.

Policymakers must work together on serious tax and entitlement reforms to put debt on a clear downward path relative to the economy and should not declare false victories while sweeping the debt issue under the rug.