Debt Ceiling Needs to be Raised in Advance of X Date

Recent reports from the Congressional Budget Office (CBO) and the Bipartisan Policy Center estimate that the debt ceiling, which was reinstated on January 2, will need to be lifted in advance of the “X date,” projected to be reached in the late summer, in order to avoid default.

Specifically, CBO estimates that the X date – the date at which the U.S. will no longer be able to complete all of its obligations on time and in full – will be reached in August or September, when the “extraordinary measures” currently being employed by the Treasury Department will be completely exhausted. In a release last week, the Bipartisan Policy Center estimated that the X date will fall between mid-July and early October.

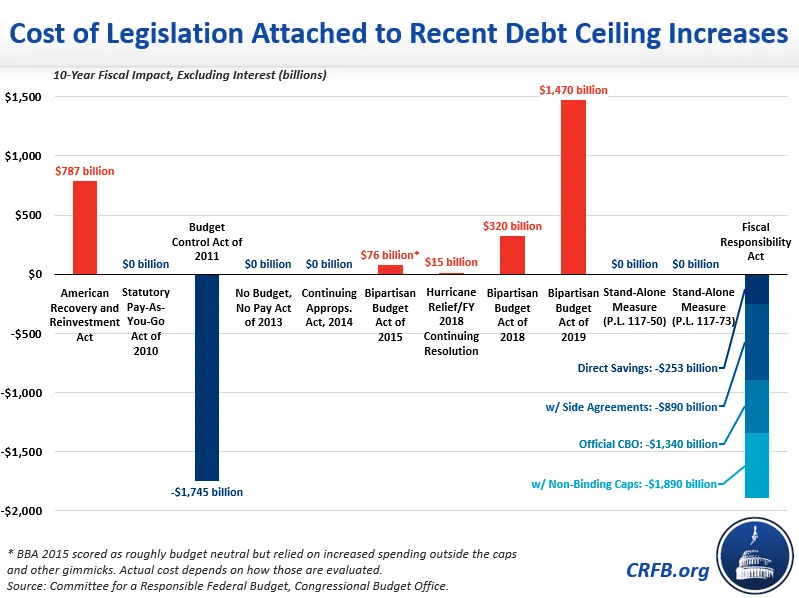

Congress most recently suspended the debt ceiling from June 2023 to January 2025 via the Fiscal Responsibility Act (FRA), which also included caps on defense and nondefense discretionary spending. CBO estimated that the FRA would reduce primary deficits by $1.3 trillion over a decade.

Ideally, Congress should once again raise or suspend the debt ceiling alongside reforms that improve the nation’s fiscal trajectory, as it has done several times in the past. At the very least, policymakers should not attach any deficit-increasing measures to a debt ceiling increase.

Select Past Debt Ceiling Increases and Their Fiscal Attachments

| Title of Bill/Package, Year | Debt Ceiling Change | Notable Attachments and Context |

|---|---|---|

| Gramm-Rudman-Hollings Act, 1985 | Increased $175B | Set targets for balanced budget, enforced by sequestration |

| Gramm-Rudman-Hollings II, 1987 | Increased to $2.8T | Built on GRH with additional deficit reduction requirements, enforced by sequestration |

| Omnibus Budget Reconciliation Act, 1990 | Increased $915B | Nearly $500 B in deficit reduction over five years, statutory PAYGO, and spending caps |

| Omnibus Budget Reconciliation Act, 1993 | Increased $600B | Reduced deficits by ~$500 B in five years, extended 1990 spending caps, raised taxes on high earners |

| Contract with America Advancement Act, 1996 | Increased $600B | Passed with POTUS line-item veto power to strike certain narrow programs and tax benefits |

| Balanced Budget Act, 1997 | Increased $450B | Put in place ~$125 B of net deficit reduction over five years and $425 B over ten years |

| Statutory PAYGO Act, 2010 | Increased $1.9T | Reinstated statutory PAYGO, informally led to establishment of Simpson-Bowles Fiscal Commission |

| Budget Control Act (BCA), 2011 | Let POTUS increase $2.1T in tranches, subject to Congressional disapproval | $917 B in deficit reduction over ten years with interest, mostly with discretionary spending caps, established the “Super Committee” to save at least $1.2 T with interest |

| No Budget, No Pay Act, 2013 | Effectively suspended to 5/19/13 | Required each chamber to pass a budget, enforced by withholding compensation of Members of Congress |

| Default Prevention Act, 2013 | Suspended to 2/7/14 | Set up a bicameral budget conference to reconcile budgets for FY 2014; ended a government shutdown |

| Bipartisan Budget Act, 2015 | Suspended to 3/15/17 | Cost ~$76 B with interest removing gimmicks, increased BCA caps for 2016 and 2017 |

| Bipartisan Budget Act, 2018 | Suspended to 3/1/19 | Cost $420 B with interest, increased BCA caps for 2018 and 2019 |

| Bipartisan Budget Act, 2019 | Suspended to 7/31/21 | Cost $1.7 T ($360 B directly) with interest, by increasing caps for 2020 and 2021 (increases were built into baseline) |

| Fiscal Responsibility Act, 2023 | Suspended to 1/1/25 | $1.5 T in deficit reduction with interest over ten years, mostly through discretionary spending caps |

Lawmakers should lift the debt ceiling as soon as possible rather than relying on extraordinary measures and waiting until the last minute. Some have suggested eliminating or reforming the debt ceiling to avoid the risk of default; there are many options to reform the debt ceiling without abandoning it altogether.

While avoiding default is necessary, it is noteworthy that the debt ceiling is one of the federal government’s few fiscal constraints. Despite its flaws, it can be used as a tool to remind us of the perilous state of federal finances and be paired with measures that improve it.

Tags

What's Next

-

Image

-

Image

-

Image