Debating Revenue Under Paul Ryan's "Roadmap for America's Future"

A month and a half ago, Representative Paul Ryan (R-WI) released his "Roadmap for America's Future," a detailed plan to reform taxes and spending, and ultimately address our long-term debt problems in full. The CBO score of the proposal found that it would significantly improve our current debt path, and eliminate the debt in its entirety by 2080. As CRFB and others praised the plan, however, some have argued its assumptions may be unrealistic -- particularly on the tax side.

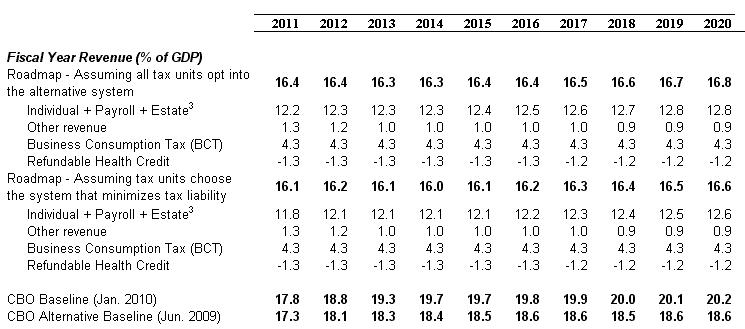

On February 4th, the Tax Policy Center's (TPC's) Howard Gleckman pointed out that CBO did not in fact truly score the revenue effects of the Roadmap. As he explained (emphasis added):

As specified by [Congressman Ryan's] staff, for this analysis total federal tax revenues are assumed to equal those under CBO’s alternative fiscal scenario (which is one interpretation of what it would mean to continue current fiscal policy) until they reach 19 percent of gross domestic product (GDP) in 2030, and to remain at that share of GDP thereafter.

[we] asked CBO to analyze the Roadmap’s long-term revenue impact and CBO declined to do so because revenue estimates are in the jurisdiction of the Joint Tax Committee (JCT). JCT does not currently produce revenue estimates beyond the traditional 10-year scoring horizon. Based on consultations with the Treasury Department and other tax experts, the Roadmap’s tax rates were formulated to produce revenues equivalent to the current tax code.

The tax reforms proposed and the rates specified were designed to maintain approximately our historic levels of revenue as a share of GDP, based on consultation with the Treasury Department and tax experts. If needed, adjustments can be easily made to the specified rates to hit the revenue targets and maximize economic growth.

Regardless of where you fall in this debate, Rep. Ryan deserves a lot of praise for putting out a detailed plan to deal with the exploding long-term debt. Very few lawmakers have proposed specific ways to deal with our debt, and Ryan has a plan to significantly curb the cost of entitlement programs and eventually bring the debt under control. But there is one lesson from this exercise -- large tax cuts (at least compared to current policy) are probably off the table for good, if we are serious about getting our fiscal house in order.

Though Ryan did not intend to do so, TPC and CBPP show that cutting taxes by about 2 percent of GDP (relative to current policy) would drive the debt to astronomical levels -- even assuming the extremely large (and extremely brave) spending cuts proposed by the Congressman.

Congressman Ryan is certainly right that "we simply cannot chase our unsustainable growth in spending with ever-higher levels of taxes," but there is a corollary. We don't appear to be able to chase our continued appetite for tax cuts with the necessary cuts in spending -- and we can't continue to finance them through borrowing.

To get our debt under control, both taxes and spending will have to be on the table. Representative Ryan deserves all the praise in the world by taking the first step, and putting forward a real and honest plan to move forward. If others want to criticize his plan for raising insufficient revenue or cutting spending too traumatically, that is fine. But it is time for them to put forward sustainable alternatives.

We look forward to seeing them.