Running on Empty? Fiscal Space and the Next Recession

The national debt increased dramatically during and after the Great Recession, rising from 35 percent of Gross Domestic Product (GDP) in 2007 to 66 percent by 2011. Though that recession was uncharacteristically large, debt has also risen in every other recession since 1970 by an average of 5 percent of GDP.

In past recessions, the country has had reasonably low debt levels, allowing us to withstand automatic increases in debt as unemployment rose and incomes fell, while also having flexibility to adopt fiscal stimulus measures to boost the economy.

Fig. 1: Debt Before and Following Recessions (Percent of GDP)

| 1973-1975 | 1980 | 1981-1982 | 1990-1991 | 2001 | 2007-2009 | |

|---|---|---|---|---|---|---|

| Pre-Recession | 25% | 25% | 26% | 39% | 34% | 35% |

| Post-Recession | 27% | 28% | 35% | 48% | 36% | 66% |

| Increase in Debt | +2% | +3% | +9% | +9% | +2% | +31% |

Sources: Office of Management and Budget, Congressional Budget Office

Pre-recession debt is in the fiscal year before the recession while post-recession debt is two years after the recession ended.

Since 1970, there has been a recession every 5 1/2 years on average. Though it is impossible to predict the timing of the next recession, the fact that one has not occurred in the last 7 years suggests one is likely on the horizon. Unless there is a dramatic reduction in debt, we will enter the next recession with the highest debt level in nearly 70 years (and higher than any time prior to World War II).

This has led to legitimate concerns about the available “fiscal space” in the United States, or the federal government’s financial capacity to respond to emergencies. While there is not a single definition of fiscal space and it is impossible to know the precise amount, the United States clearly has less fiscal space today than it did a decade ago and is projected to have less in the years to come.

As a result, the United States is more poorly equipped to handle the next recession than it was to handle the most recent one. This reality is even more troubling because the Federal Reserve has less monetary space due to already-low interest rates and a very large Federal Reserve balance sheet.

Our simulations show that in ten years, a recession could lift debt levels to within 8 to 17 percentage points of GDP of the country’s all-time record high debt levels set after World War II, leaving less capacity for fiscal stimulus than was available during the Great Recession.

In order to create the necessary fiscal space, policymakers should enact an agenda that slows the growth of federal debt while accelerating economic growth.

The United States Faces Diminished Fiscal and Monetary Space

One measure of a country’s preparedness for national crises like recessions or war is the capacity to expend resources in an emergency. When talking about debt, this capacity can be measured as “fiscal space,” the amount a government can borrow, and “monetary space,” the amount a government or its central bank can expand the money supply.

It is impossible to know exactly how much fiscal and monetary capacity the U.S. government has. There is not an exact threshold above which economists know debt can no longer rise. Nor does monetary space have a hard cutoff; new experiments with balance sheet operations and negative interest rates suggest the bounds of monetary policy aren’t simple either.

Moreover, there is no one definition of fiscal space – it may refer to the amount of additional borrowing possible before default is likely but also can mean the amount of borrowing before a fiscal crisis ensues, economic growth noticeably slows, a debt spiral becomes inevitable, debt reduction becomes unachievable without damaging austerity measures, or the political system no longer supports more borrowing.

Yet while total available fiscal and monetary space is unknown, there is certainly less of it today than just a decade ago. On the monetary side, the Federal Reserve has fewer options than it did before the Great Recession in 2007.

The Federal Reserve can typically boost economic activity by reducing interest rates and expanding its balance sheet. In 2007, the federal funds interest rate was 5.25 percent compared to 0.25 to 0.5 percent today. Assuming a 0 percent lower bound (though the actual bound is likely a bit lower), the Federal Reserve would have been able to stimulate the economy with rate cuts of at least 500 basis points in 2007 – but today could pursue a rate cut less than a tenth as large.

Fig. 2: Metrics of Fiscal and Monetary Space

| 2007 | 2016 | |

|---|---|---|

| Federal Funds Rate | 5.25% | 0.25-0.5% |

| Federal Reserve Balance Sheet | $850 billion* | $4.5 trillion |

| Share of Balance Sheet in Short-Term Treasuries | 90% | 12% |

| Federal Debt Held by the Public (% of GDP) | 35% | 77% |

| Projected Debt in Ten Years (% of GDP) | 45%^ | 86% |

Sources: Federal Reserve, Congressional Budget Office

*Size of balance sheet prior to first federal funds rate cut in September 2007

^Taken from the Alternative Fiscal Scenario in CBO’s 2007 Long-Term Budget Outlook

The Federal Reserve also had a balance sheet of $850 billion in 2007, almost entirely in short-term Treasury securities, which it expanded considerably in response to the recession. Now its balance sheet of $4.5 trillion is made up largely of long-term Treasury bonds and mortgage-backed securities. The Federal Reserve still has several tools at its disposal to help manage an economic downturn, but they are fewer and have a more uncertain impact than the ones available in 2007.

The United States faces a similar situation in terms of fiscal space. Typically, during a recession, the country can boost economic activity by enacting deficit-financed tax cuts and spending increases. The traditional automatic stabilizer programs already in place like unemployment insurance as well as discretionary stimulus contributes to the recovery. Stimulus, however, may become less affordable as debt increases.

In September 2007, debt held by the public totaled roughly $5 trillion, or 35 percent of GDP. This was around the historic average at the time, 71 percent of GDP below the country’s all-time record set after World War II, and 25 percent of GDP lower than the limit of the European Union’s Maastricht Treaty sets for member countries (60 percent). As a result, the United States had significant fiscal space to not only absorb the direct economic cost of the Great Recession but also enact significant financial and fiscal stimulus measures. A similar response may not be possible (or may not be as easy to enact) in the future, as the Congressional Budget Office (CBO) explains:

Before the most recent recession, when federal debt was below 40 percent of GDP, the government had some flexibility to respond to the financial crisis and severe recession with policy changes…If federal debt stayed [at today’s level] or increased further in the future, undertaking similar policies in recessions or fiscal crises would be harder. Hence, such developments could have larger negative effects on the economy and on people’s well-being.

For illustrative purposes, one way to show fiscal space would be to measure how close the debt is to the all-time record debt level of 106 percent of GDP set in 1946. This level could represent a hypothetical political limitation on debt and would be a move into uncharted territory.

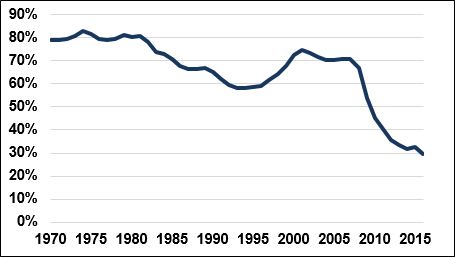

Fig. 3: Illustrative “Fiscal Space” to Record-High Debt, 1970-2016 (Percent of GDP)

Source: Congressional Budget Office

Using this illustrative measure, available fiscal space generally totaled between 60 and 80 percent of GDP before the Great Recession, but has fallen from 70 percent of GDP in 2007 to only 29 percent of GDP today. This suggests the country has significantly reduced borrowing capacity for the next major war, recession, or other national crisis.

Fiscal Space Could Decline Rapidly in the Next Recession

Recessions in the United States have occurred on average every 5 1/2 years since 1970, and it has been seven years since the last one. Yet typical budget projections like those from the CBO do not account for what might happen when the next recession occurs (nor, in fairness, what would happen in the next boom).1

To illustrate our declining fiscal space, we ran two debt simulations showing what would happen if a recession started in 2018. In the first situation, we assumed a “typical” recession with a typical drop in revenue, increase in automatic stabilizers, reduction in GDP (relative to potential GDP), and eventual recovery based on the average effects of all recessions between 1973 and 2001. We then simulated a “large recession” based on the recent Great Recession’s direct cyclical effects but without any lasting effects on productivity or labor force participation. These simulations did not assume any budgetary cost associated with economic stimulus or financial rescue packages (though they implicitly incorporate the economic boost that resulted).

Based on these simulations, we find that debt would rise considerably. In the case of a typical recession, debt would reach 89 percent of GDP in 2026, compared to 86 percent under current law. Meanwhile, a large recession could cause debt to reach 98 percent of GDP by 2026. Either of these scenarios would mean less fiscal space than is available today.

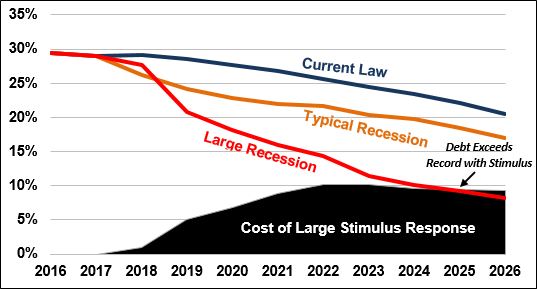

Fig. 4: Illustrative “Fiscal Space” to Debt Record and Recession Response (Percent of GDP)

Source: CRFB calculations based on Congressional Budget Office data

Under our illustrative measure, which shows fiscal space until debt reaches record levels, we find that fiscal space would decline to 17 percent of GDP by 2026 with a typical recession and only 8 percent of GDP in the case of a large recession.

Implementing the level of stimulus and financial rescue measures put forward in the Great Recession, for example, would cost 9 percent of GDP by 2026, enough to consume all the fiscal space remaining before debt exceeded its World War II-era record-high level. This could result in serious political and possibly even economic constraints to enacting stimulus measures.

In other words, another large recession would limit the government’s ability to stimulate the economy without bringing debt above record-high levels.

It is difficult to know when a country will run into problems. We used 106 percent purely as an illustration. But whatever the threshold, higher debt will bring the country closer to its maximum capacity.

Conclusion

Having sufficient fiscal space is important to give the federal government flexibility to respond to emergencies and other needs. It is difficult to know how much fiscal space the United States currently has, but the recent run-up in debt has put the federal government in mostly uncharted territory. For that reason, it has become at least a little more likely that the federal government’s fiscal capacity will not be sufficient when substantial new borrowing is needed.

Lawmakers should work to reduce the current projected high level of debt (as a percent of GDP), rather than letting it rise unsustainably, in part to help provide enough fiscal space to respond to new needs and emergencies. Even reducing the future debt relative to the economy may create more fiscal space today by re-assuring markets and policymakers about the long-term sustainability of the country’s fiscal situation.

High and rising levels of debt can tie the hands of policymakers, making it more difficult for the government to respond to important national needs, particularly during an economic downturn. President John F. Kennedy once said, “the time to repair a roof is when the sun is shining.” The time to fix the debt and to ensure we have the fiscal space to respond to emergencies is now.

1 Rather than try to project what the next business cycle will look like – a nearly impossible task – CBO’s longer-term economic projection is an average estimate that incorporates the possibility of recessions as well as economic booms. Because the economy on average has run below potential for deeper and/or longer than it has been above it, CBO assumes GDP remains about 0.5 percent below potential.