Understanding the Health Insurance Excise Tax

The health care reform bill recently passed by the Senate Finance Committee relies on a $200 billion health insurance tax to help fund the costs of expanding health insurance coverage. Although there are some exceptions, the policy generally imposes a 40% excise tax on each dollar of health insurance premium beyond $8,000 for an individual or $21,000 for a family.

Although this tax is far from perfect (limiting the employer sponsored insurance tax exclusion directly would probably be better), it has at least two major advantages in the context of health reform: it grows faster than new health care costs and it helps to slow health care cost growth.

A Growing Revenue Sources

The excise tax offers a growing source of revenue. This is because the $8,000/$21,000 threshold is only indexed to 1% above inflation (CPI+1), but actual health insurance costs are projected to grow much faster. As a result, according to the Joint Committee on Taxation (JCT), the percent of premiums affected by the tax would increase from 4% in 2013 to 11% in 2019.

The importance of having a rapidly growing set of offsets in the health care bill should not be understated. Since the costs of coverage expansion itself must grow to keep pace with premium costs, they have the potential to add significantly to the deficit beyond the ten-year window. This is the case in the House bill, which relies largely on an income surtax to finance its costs.

Annual Growth of Coverage Provisions and Income Surtax in House Tri-Committee bill (billions)

Sources: Congressional Budget Office, Joint Committee on Taxation, and CRFB Calculations

The Finance bill, meanwhile, is actually projected to reduce the deficit in the second decade by between ¼ and ½ of GDP - in no small part due to revenues from the excise tax growing faster than the costs of coverage expansion.

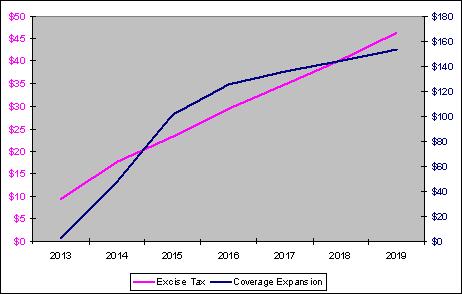

Annual Growth of Coverage Provisions and Health Insurance Excise Tax in Senate Finance bill (billions)

Sources: Congressional Budget Office, Joint Committee on Taxation, and CRFB Calculations

A Potential Curve Bender

In addition to being a growing source of revenue, the excise tax could actually help to reduce overall health care costs. Currently, because compensation in the form of health insurance is untaxed, employers provide a disproportionate amount of compensation in the form of insurance - which in turn helps to drive up health care costs. By taxing high-cost insurance, though, the incentives reverse. As we explained in Evaluating Health Care Costs:

The excise tax would increase the price of high-cost insurance, leading to seek out more efficient and less generous insurance. Doing so would drive down both health care prices and utilization, slowing system-wide health care cost growth.

The Lewin Group modeled a similar (but much more aggressive) policy --- capping the health insurance tax exclusion for high earners and expensive plans --- and found that while the plan would raise $760 billion over ten years, it would also reduce national health spending by $280 billion.

So Where Does the Money Come From?

While the Finance Committee's excise tax has the benefits of both growing faster than the bill's costs and helping to slow health care cost growth, it is no free lunch. And although the tax is technically imposed on insurance companies, the vast majority of it will be passed along to consumers in the form of higher insurance premiums.

At that point, employers and employees will face a choice: either pay the higher premiums, or accept lower-cost insurance benefits in place of higher cash wages - which are subject to normal taxation. According to JCT's estimates, most will do the latter.

Of the $201 billion in revenue JCT estimates the excise tax will generate, only $38 billion - less than 20% - would come from the excise tax itself. The lion's share of the revenue would come from the income tax - as firms began offering higher wages in exchange for providing less generous health insurance benefits. A substantial portion of the revenue would also come from Social Security payroll taxes; this revenue would technically go into the Social Security trust funds, modestly improving the system's cash balance in the short run, but resulting in higher future benefits.

Source of Revenue from Excise Tax through 2019 (billions)

Source: Joint Committee on Taxation

*also includes impact of other on-budget taxes such as the Medicare payroll tax

The fact that most revenue from the excise tax would come as a result of higher cash wages strengthens the thesis that the excise tax could slow health care cost growth. Although cheaper insurance need not mean less health care spending, there is certainly a strong correlation between the two.

This is not to suggest that the excise tax is a perfect policy - in fact it is far from it. It is also not to suggest that the excise tax would do even nearly enough to slow health care cost growth - much more is needed.

But given its benefits, policy makers should think twice about abandoning or diluting it, unless they are willing to replace it with something better.