Senator Rand Paul Releases Flat Tax Plan

This blog is part of a series of "Policy Explainers" for the 2016 presidential election, where we explain some of the candidates' policy proposals that affect the federal budget.

Republican Presidential candidate Senator Rand Paul (R-KY) recently released his Fair and Flat Tax Plan. His plan would dramatically overhaul the tax code by eliminating most preferences and replacing existing income taxes with a 14.5 percent flat tax for individuals, businesses, and investments. He would also eliminate other taxes including payroll taxes, estate taxes, and tariffs. Two outside groups have evaluated the costs of his plan, finding a wide range of revenue losses between $1.8 trillion and $15 trillion.

Individual Income Tax Reform

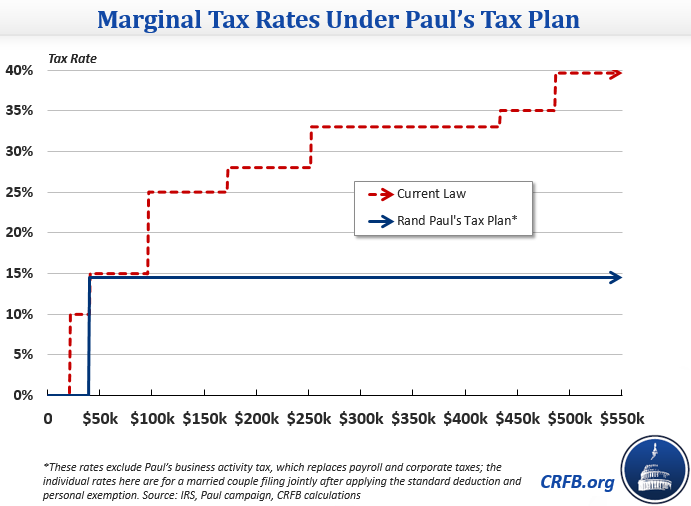

On the individual side, the 14.5 percent flat tax would apply to wages, salaries, dividends, capital gains, rents, and interest. The plan would maintain the mortgage interest deduction, charitable deduction, the Earned Income Tax Credit, and the Child Tax Credit. It would increase the standard deduction and dependent exemption in such a way that a family of four would not be taxed on its first $50,000 of income (up from $28,600 now). By providing one flat rate of 14.5 percent, taxpayers currently in the 15 percent bracket would only see a very small reduction in their marginal rates, while the rates of the highest income individuals would fall by over 25 points.

In addition to lower rates, the plan identifies several other tax cuts including:

- Repealing the Alternative Minimum Tax (a default effect of applying a flat 14.5% tax on all income)

- Repealing estate and gift taxes

- Increasing the personal exemption to $5,000 per person

- Increasing the standard deduction to $15,000 per filer ($30,000 for joint filers)

Paul says that he would cover the revenue loss and then some with spending cuts, and indeed he has proposed enough in the Senate to do that. For example, his proposed budget from 2013 that called for $7.3 trillion in spending cuts.

Corporate Income Tax Reform

A notable feature of Paul's plan is that it eliminates corporate and payroll taxes, replacing them with a flat 14.5 percent "business-activity tax" (BAT). This tax has two main differences from the current corporate income tax: capital expenses would be deducted immediately instead of depreciated over time, and wages would no longer be deductible, so all employers, even nonprofits and governments which don't normally pay income tax, would pay a 14.5 percent tax on wages.

Making wages non-deductible has a huge impact on revenue, since it essentially means most wage income would be taxed twice under Paul's plan -- once at the business level and again at the individual level. This feature, in combination with full deductibility of all non-wage business expenses (ex: capital investments), effectively makes the BAT into a consumption tax. In fact,some commentators have described Paul's plan as a value-added tax (VAT). There is something to this claim, though unlike European-style VATs, Paul's tax would not be imposed at each stage of production nor appear as a tax at the point of consumption.

The tax would also come in place of a 35% corporate income tax, a 12.4% Social Security payroll tax on a worker's first $118,500 of wages, and a 2.9 to 3.8 percent Medicare tax on all wages. Both payroll taxes are split evenly between employer and employee.

Revenue Impact

The two estimates on the fiscal impact of Paul's plan vary widely. The right-leaning Tax Foundation has a static score showing $1.8 trillion in revenue loss over ten years. Their dynamic estimate, which accounts for effects of economic growth, predicts the plan will increase the size of the economy by 12.9 percent over ten years and shows a $737 billion ten-year revenue gain. Sen. Paul states that his plan is not intended to be revenue-neutral but rather would provide "an over $2 trillion tax cut," which appears to be based on the Tax Foundation's static estimate.

The other estimate comes from the left-leaning Citizens for Tax Justice, which finds a much larger static revenue loss. In 2016 alone, they found that the plan would lose $1.2 trillion – $700 billion from the individual income tax changes and $500 billion from the corporate and other changes. Over ten years, Citizens for Tax Justice expects the plan to lose $15 trillion.

For its part, the Tax Foundation argues (based on numbers from the Tax Policy Center) that Citizens for Tax Justice underestimates potential VAT revenues by about half. From the other side, Citizens for Tax Justice claims that the Tax Foundation understates the cost of corporate rate cuts. Ultimately, if the plan were taken up in Congress, the only estimate that would matter is the one from the Joint Committee on Taxation, the official scorekeeper for revenue bills.

| Economic and Revenue Analysis of Sen. Paul's "Fair and Flat Tax Plan" | |||

| Tax Foundation | Citizens for Tax Justice | ||

| Revenue Impact | Ten-Year Cost | ||

| Conventional Score (no economic growth) | -$1.8 trillion | -$15 trillion | |

| Dynamic Score | +$0.7 billion | N/A | |

| Economic Growth from Tax Reform Alone | |||

| Increase in GDP by the 10th Year | 12.9% | N/A | |

| Average Increase in GDP over the next 10 years | 6.4% | N/A | |

Sources: Tax Foundation, Citizens for Tax Justice

Conclusion

Senator Paul’s plan for tax reform would dramatically simplify the tax code. However, under traditional static scoring, Paul’s plan would lose at least $1.8 trillion in tax revenues. Paul has promised to offset the cost with spending cuts akin to the measures he has introduced in the Senate. We hope that Senator Paul will soon describe these spending cuts that will prevent his tax plan from adding to the national debt.