Myth Buster: Other Plans are Much Worse Than the Fiscal Cliff

We've shown that there a plenty of reasons to not go over the fiscal cliff, including that it implements fiscal consolidation in an abrupt and blunt way causing a recession and puts a great deal of strain on the poor. We also know that we cannot just repeal the cliff without any offsets, since that would be a clear signal to the markets and public that even after numerous showdowns and negotiations, lawmakers cannot make sufficient progress on solving our fiscal issues.

But some commentators have argued that for the poor, the plans that would replace the cliff would be much worse than the cliff itself. While we cannot be sure what the final terms of a deal between Democrats and Republicans would be, we can look to bipartisan proposals such as Domenici-Rivlin and Simpson-Bowles as a guide. By many measures, these plans do a much better job at protecting the most vulnerable.

Revenue Increases are More Progressive

On taxes, most economists agree that, all else equal, having a broader base and lower marginal tax rates is preferable. The lower rates in tax reform have prompted some commentators to say that these reform plans will primarily benefit the rich, but Tax Policy Center distributional analysis of both the Domenici-Rivlin and Simpson-Bowles plans are more progressive than the fiscal cliff. That's because many of the tax expenditures that tax reform would reduce or eliminate overwhelmingly benefit the wealthy.

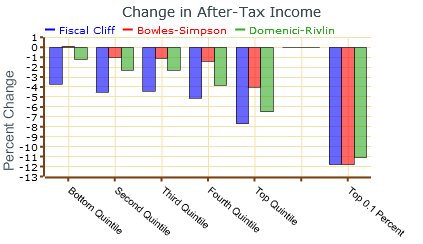

The graph below shows the change in after-tax income from each plan and the fiscal cliff compared to continuation of current policy.

As can be seen above, despite reducing tax rates from current levels the Simpson-Bowles and Domenici-Rivlin plans raise substantial net revenue and do so in a far more progressive way than under the fiscal cliff (which increases rates). Going over the fiscal cliff means letting the 10% bracket increase to 15%, the $1,000 child credit reduce to $500 and lose most of its refundability, and a host of other taxes to go up on the poor and middle class. According to Tax Policy Center, in fact, the bottom quintile will see their aftertax income fall by almost 4 percent, and the second quintile by over 4 percent.

By comparison, the Simpson-Bowles and Domenici-Rivlin plans raise only very modest amounts of money from those in the bottom half of the income spectrum, with most new revenue being raised from the top quintile and especially from the top 1 percent.

Spending Cuts Designed to Protect Low Income

We've already refuted the claim that the most vulnerable are protected from the sequester in the fiscal cliff -- indeed they are hit quite hard, especially when compared to what would occur under bipartisan deficit reduction plan. True, the fiscal cliff does exempt low-income mandatory programs from cuts, but so do the bipartisan deficit reduction plans out there. A key principle in Simpson-Bowles was to "protect the most vulnerable," and neither it nor Domenici-Rivlin touch food stamps, Supplemental Security Income, unemployment insurance, or similar programs.

Where the sequester really hits low-income programs is on the discretionary side. More than one quarter of domestic discretionary spending goes to low-income programs like section 8 housing and low-income heating assistance. That means they could take a $120 billion hit under the sequester over ten years. By comparison, any bipartisan plan which calls for additional discretionary reductions will most certainly do what Simpson-Bowles and Domenici-Rivlin did and achieve those savings with caps. Those caps are very unlikely to be as deep as the sequester, and even if they were they have the advantage of allowing appropriators to assign reductions where it makes sense rather than across-the-board.

On health care, any bipartisan plan is likely to have deeper reductions than the fiscal cliff. But as we've showed before, there are any number of health care reforms that can promote greater efficiency in Medicare and Medicaid without harming the poor.

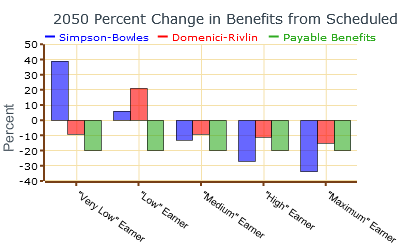

And then there is the question of Social Security. The fiscal cliff leaves Social Security insolvent, which would lead to beneficiaries receiving a benefit cut of 25 percent in 2033 if no action is taken. On the other hand, both Simpson-Bowles and Domenici-Rivlin propose a combination of new revenue, mostly progressive benefit changes, and new minimum benefits which protect and in some cases enhance benefits for low-income beneficiaries. Indeed, compared to a no-action baseline ("payable benefits" below), both plans do quite well.

Source: Social Security Administration

Note: Benefit calculations assume longest number of years worked for each earner (30 or 44 years) since they are the most common according to SSA

Growth is Stronger under a Replacement Plan

We've shown before in this Myth Busters series how the fiscal cliff would devastate the economy in the short run. But by implementing more gradual reduction, we can have stronger economic performance compared to going over the cliff.

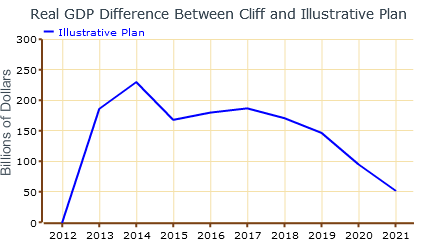

Macroeconomic Advisors recently modeled the fiscal cliff against a relatively modest illustrative plan. Their finding was that a plan which gradually stabilized the debt -- even at a high level -- was far better for the economy than the fiscal cliff in the short term. Over the long-run, the deficit reduction from the fiscal cliff does improve the growth trend relative to the illustrative plan, but it takes many years to catch up. Thus, the Macroeconomic Advisers data show the importance of timing in deficit reduction.

A plan with more, but equally gradual, deficit reduction than the illustrative plan they modeled would likely have similar effects in the short-term and much more positive effects over the longer term. This would be especially true for plans like Simpson-Bowles and Domenici-Rivlin, which include specific growth enhancing policies such as base-broadning rate-reducing tax reform, new initiatives to increase public investments, and incentives to encourage people to work longer.

Any bipartisan plan to gradually reduce the debt will almost certainly be better in the short and medium term for the economy than the fiscal cliff, and is likely to be better for the long term as well. Faster growth means more jobs and higher wages.

There is no question that whatever plan is enacted will have its critics. Advocates and interest groups may think a plan went too far in one area or another. But a comprehensive plan would most definitely be an improvement over the fiscal cliff.

What's Next

-

Image

-

Image

-