JCT: Tax Cuts 2.0 Would Slow Long-Term Economic Growth

The Joint Committee on Taxation (JCT) has released an official dynamic score of "Tax Reform 2.0" – a bill permanently extending last December's tax cuts past their 2025 expiration. JCT estimates that the legislation would increase the size of the economy by about 0.5 percent in the years immediately after the cuts are extended (a roughly 0.05 percentage point increase in the average growth rate for the decade), but it would slow economic growth over the long term. The result of this faster near-term growth would be to generate budget savings of $86 billion of "feedback" revenue, enough to offset 14 percent of the $631 billion conventional cost of the bill. As a result, the bill would cost $545 billion over a decade and more than $200 billion per year once in effect.

Most outside estimators agree with JCT's findings: extending the individual provisions of the tax bill will cost nearly $650 billion through 2028 on a conventional basis, and dynamic growth effects will offset no more than one-seventh of the cost. Whereas JCT estimates $86 billion of dynamic feedback, the Tax Policy Center (TPC) estimates $71 billion, the Tax Foundation estimates $62 billion, and the Penn Wharton Budget Model (PWBM) estimates that the dynamic feedback would be negligible.

| Organization | Conventional Score | Dynamic Boost | Dynamic Estimate |

|---|---|---|---|

| Joint Committee on Taxation | -$631 billion | $86 billion | -$545 billion |

| Tax Policy Center | -$642 billion | $71 billion | -$572 billion |

| Tax Foundation | -$638 billion | $62 billion | -$576 billion |

| Penn Wharton Budget Model1 | -$626 billion | $5 billion to -$13 billion | -$621-$639 billion |

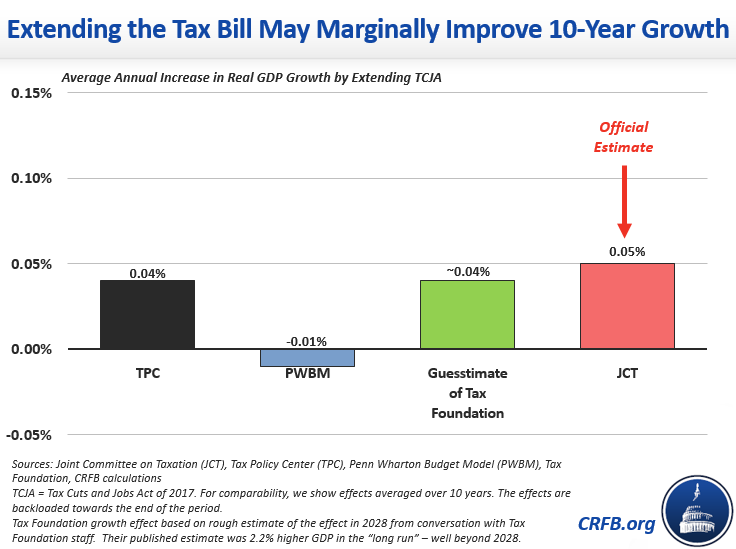

Similarly, three of the four estimators find that extending these provisions will modestly improve economic growth over the next decade. Whereas JCT's estimates suggest the economy would grow about 0.05 percentage points faster through 2028, TPC and Tax Foundation2 estimate 0.04 points faster growth. PWBM, on the other hand, projects 0.01 percent slower growth annually.

Importantly, even this modest improvement in growth is unlikely to last due to the negative effects of higher debt. We previously estimated that "Tax Reform 2.0" would cost $4 trillion ($5 trillion with interest) over the next decade. The Tax Policy Center and Penn Wharton Budget Model have reached similar conclusions. This massive debt increase is likely to crowd out private investment and thus slow economic growth over the long term. According to JCT:

Absent some offsetting change in fiscal policy, government debt is expected to begin requiring increasing shares of economic resources, reducing resources available for private investment. Measured relative to the April 2018 CBO baseline, in the decades after 2028, private capital investment and GDP growth are projected to slow. While employment is expected to continue to be above baseline projections, GDP is projected to become lower under the proposal than under CBO’s April 2018 baseline in the decades after 2028; revenue feedback from the policy would decline commensurately.

Both TPC and PWBM – who also account for the costs of debt – agree that any pro-growth effects from lower tax rates will ultimately be countered by higher debt. TPC estimates the 0.5 percent GDP boost in 2026 will fall to only 0.1 percent by 2038, while PWBM estimates that GDP would be 0.6 to 0.9 percent lower by 2040 as a result of the tax bill. Only the Tax Foundation, whose model does not account for the cost of debt, finds that extending the tax cuts will provide a permanent boost to the economy.

Unfortunately, the tax bill will add significantly to an already dismal debt situation – even after accounting for economic growth. And ultimately, the bill will have little or negative effect on GDP over the medium and long terms. Making the whole bill permanent would help to improve its effect on ten-year growth, but at the cost of significantly more debt that would ultimately slow growth in the long term.

To truly improve economic growth, lawmakers should fix the tax bill rather than simply extending it. That means paying for any extensions, closing loopholes, and offsetting the fiscal damage from the recent tax cuts by reducing tax breaks or spending. Lawmakers must also pursue a series of economic, fiscal, and labor market reforms outside of the tax code. That will involve addressing the underlying structural imbalances through long-term entitlement reforms to make Social Security and Medicare solvent and put our nation's fiscal trajectory on a sustainable path.

1 The Penn Wharton Budget Model did not provide a dynamic score with their most recent estimate through 2028. The table lists the dynamic effects through 2027 from an earlier April 2018 estimate. For comparability with the other estimates, we removed two provisions included in other bills -- a deduction for start-up costs and universal savings accounts.

2 The Tax Foundation average annual growth effect is an estimate based on conversations with Tax Foundation staff. Their published estimate is that the bill will boost long-run GDP by 2.2 percent, but that is for a period beyond 2028.

What's Next

-

Image

-

Image

-