How Other Countries Have Regained AAA Ratings

Over at Ezra Klein's blog, Sarah Kliff writes about the "Maple Leaf Miracle," or how Canada was able to turn itself around after it was downgraded. Considering our current situation, it seems appropriate to revisit the countries that we talked in our paper on fiscal turnarounds last year and see how well they line up with our table released the other day of countries that have lost their AAA credit rating only to regain it at a later time.

Our fiscal turnarounds paper went into four countries' fall from grace and subsequent rebound: the aforementioned Canada, Denmark, Finland, and Sweden. We also talked about Ireland, but they have fallen on hard times again in the wake of the 2008 financial crisis and have yet to rebound.

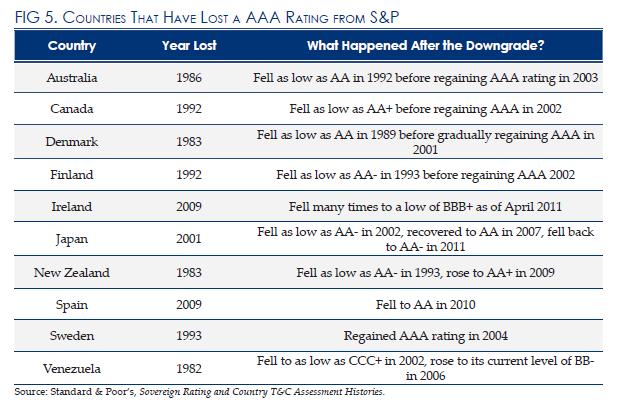

The table below is from our paper on the S&P downgrade, detailing all the countries that have been downgraded from AAA by S&P. After the table is a detailed summary of the four countries' journey from AAA and back.

- Canada: After years of running deficits, Canada suffered from a high and mounting debt. After the Mexican peso crisis in 1994, Canada was seen as next on the global "chopping block," and after Moody's downgraded Canada from AAA in 1995 (with debt at 70 percent of GDP), our neighbors to the north decided to act on their fiscal imbalance. Most of the fiscal adjustment came on the spending side, with cuts to civil service, wage freezes, transfer of some responsibilities to provinces, and other program reductions. Aided by the slide of Canadian dollar against the U.S. dollar--which boosted Canadian exports--and the general economic boom in the mid- to late-1990s, the measures worked, returning surpluses to the Canadian budget in the late 90s and returning Canada to AAA status in 2002.

- Denmark: In Denmark's case, they experienced a serious fiscal deterioration as a result of the early 1980s recession; public debt rose from 29 percent of GDP in 1980 to 65 percent in 1982. In addition, in an environment of high interest rates, the interest costs on that increased debt were also severe. Faced with a downgrade from S&P in 1983, Denmark undertook a huge fiscal consolidation plan, which relied on revenue for a little more than half of the deficit reduction. Also, many benefit and transfer programs were cut. As a result, the sharp rise in debt was halted by the middle part of the decade. A further deficit reduction program put debt on a declining path in the 1990s, and Denmark regained its AAA rating with S&P in 2001.

- Finland: Finland had a banking crisis in the early 1990s that led to a severe recession. The annual fiscal balance swung from 6 percent of GDP surpluses before the crisis to an 8 percent deficit in 1993. Government debt shot up 50 percentage points of GDP from 1990 to 1994 (10 to 60), and S&P downgraded the country in 1992. In response to both the banking and the fiscal crisis, Finland took many steps. They attempted to shore up the banks by issuing a blanket guarantee of deposits; also, they injected capital into banks or took them over when necessary. On the fiscal side, much of the adjustment was on the spending side, including reforms to many entitlements. However, the consolidation effort also included some tax base broadening and the introduction of a value-added tax (VAT). As with many deficit reduction efforts, the plan was helped by a devaluation of the currency that increased global competitiveness. The efforts helped stabilize, then reduce, the debt path of Finland, returning them to surpluses in the late 1990s. They regained their AAA rating in 2002.

- Sweden: Sweden faced a similar situation to Finland. Financial problems lead to fiscal problems in the early 1990s. As a result of the financial crisis, Sweden turned to fiscal expansion, partially through efforts to shore up the banking sector, which resulted in spending rising from 59 percent of GDP in 1990 to 70 percent in 1993 (while revenue stayed at 59 percent of GDP). Sweden was hit with a downgrade in 1993 and turned to fiscal consolidation in 1994. Much of the adjustment was to a wide variety of social benefits, although increased income and payroll taxes were also involved. Again, an exchange rate that helped boost Swedish exports played a role in diminishing the contractionary effects of the deficit reduction. The combination of economic recovery and fiscal consolidation put debt on a declining path as of the mid 1990s, while the fiscal balance went from an 11 percent of GDP deficit in 1994 to a 5 percent surplus in 2000. Sweden regained their rating in 2004.

These countries faced broader concerns about their fiscal position, yet were still able to turn things around and regain their fiscal credibility. The U.S. has only been downgraded by one major credit rating agency, and we still have time to make the necessary adjustments without the context of a crisis. But we have to get going on a comprehensive plan.

To read our fiscal turnarounds paper, click here.

To understand the S&P downgrade, click here.