Why Should We Worry About the National Debt?

Though the national debt is at a post-war high, the willingness of policymakers to address it seems as if it is at an all-time low. The last two years have been defined by massive, unpaid-for tax cuts and spending increases, with little attention to addressing near- or long-term fiscal imbalances.

Meanwhile, commenters on the left and right are increasingly urging Washington to ignore mounting debt levels and instead focus on enacting new costly initiatives while protecting special interest tax breaks and spending programs.

This new debt denialism could not come at a worse time. The rapid aging of the population means that deficits and debt are on course to explode in the coming decades. With a strong economy and unemployment rate below 4 percent, now is the time to begin reducing deficits, not increasing them. As President John F. Kennedy once said, “the time to repair the roof is when the sun is shining.”

Yet instead of repairing our fiscal situation, policymakers seem intent on worsening it. Never have deficits been this high when the economy was this strong – and they are growing. We project debt held by the public as a share of the economy will double by mid-century under current law, from 78 percent of Gross Domestic Product (GDP) today to over 150 percent by 2050. Extending current policy, we project debt will rise above 205 percent of GDP by 2050 – nearly twice its historic record.

The consequences of such high and rising debt could be significant. In this paper, we explain that high and rising debt will:

- Slow income growth;

- Increase interest payments, crowding out other priorities;

- Push up interest rates;

- Dampen our ability to respond to the next recession or emergency;

- Place more burden on future generations; and

- Increase the risk of a fiscal crisis.

This paper describes these consequences and will be followed by further analysis going into more detail. This paper also includes a Q&A in response to some claims that debt does not matter.

While the economy is strong today, policymakers ignore debt at their own peril. Debt cannot continue to rise indefinitely but can cause significant damage as it grows.

Rising Debt Slows Income Growth

One key consequence of rising debt is that it slows economic growth, which in turn slows the growth of wages and income.

This slower growth occurs mainly due to the phenomenon known as “crowd out,” whereby investors purchase government debt at the expense of making productive investments in private capital. Less investment ultimately means fewer buildings, machinery, equipment, and software and even fewer new ventures or technologies. As a result, workers’ productivity growth will suffer, and ultimately income and wage growth will slow.

The Congressional Budget Office (CBO) has estimated that each $1 of new borrowing reduces total investment by 33 cents, shifting an additional 24 cents of investment from Americans to foreigners who then benefit from much of the returns. A more recent CBO working paper suggests the amount of crowd out is even higher.

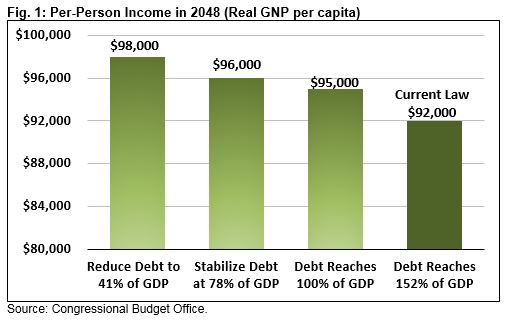

Over time, lower investment leads to slower income growth. In a recent analysis, CBO projected Gross National Product (GNP) per person – a rough proxy for average income per person – will total about $98,000 in 2048 in today’s dollars if debt is reduced to historical levels. Under current law, where debt rises to about 150 percent of GDP, average income per person will total $92,000.

In other words, rising debt will reduce income per person by $6,000, or 6 percent, compared to if debt were falling relative to the economy.

With income growth already expected to slow, it would be unwise to further worsen this trend by increasing the national debt.

Rising Debt Increases Interest Payments

As the federal debt rises, so will the cost of servicing that debt through interest payments.

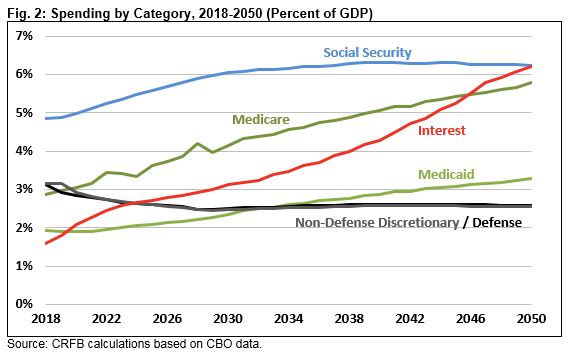

In 2018, the federal government paid 1.6 percent of GDP for debt service. Going forward, interest is projected to be the single fastest-growing part of the budget. Under current law, CBO projects interest payments as a share of the economy will nearly double to 3.0 percent of GDP by 2029; we project they’ll double again to 6.3 percent of GDP by 2050. Under CBO’s Alternative Fiscal Scenario, interest will grow even faster, reaching 3.4 percent of GDP by 2029 and 8.5 percent by 2050 under our projections. For perspective, the previous record-high is 3.2 percent of GDP.

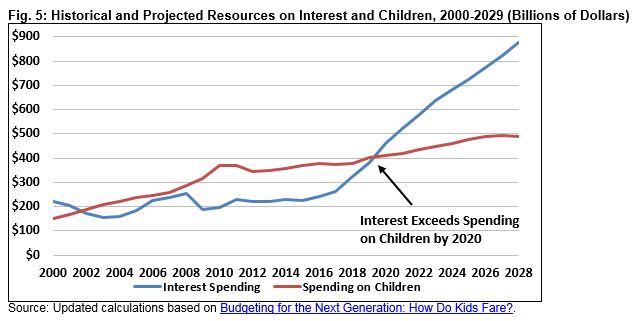

Over time, interest spending will eclipse spending on other programs. Under current law, interest payments on the debt will exceed the cost of Medicaid by 2020 and spending on defense by 2025, and it will be the single largest government expenditure after 2050.

Framed a different way, interest payments already consume every dollar raised by the corporate income tax, the estate tax, gift taxes, and federal excise taxes. By the late 2040s, under current law interest costs will consume all payroll tax revenue.

The more that is paid on interest, the less that is available to fund other priorities or the more that must be raised through additional taxes or borrowing. Rising interest costs mean less opportunity to invest in the country’s future, combat important long-term threats like climate change, maintain a strong national defense, or enact important new social spending and tax relief. Every dollar spent on interest is a dollar unavailable for something else.

Rising Debt Pushes Up Interest Rates

Another important consequence of rising national debt is the overall increase in interest rates throughout the economy.

As the government issues more bonds, lenders are likely to demand higher interest rates to compete with other investment opportunities. These higher rates are likely to permeate through the rest of the economy, increasing the interest costs associated with mortgages, car loans, student loans, and credit card debt – not to mention business loans.

While the claim that high debt leads to higher interest rates may seem suspect given today’s low rates, a substantial body of literature finds evidence that the link is strong. Today’s low interest rates are largely the result of a slowdown in economic growth, unconventional monetary policy, and increased foreign demand for safe assets; high debt has pushed interest rates up. A recent analysis by Edward Gamber and John Seliski at CBO found that each 10 percent of GDP increase in the national debt results in a 0.2 to 0.3 percentage-point increase in interest rates. Another study by economist Ernie Tedeschi, focused largely on post-recession data, estimates each percent of GDP increase in annual deficits increases interest rates by 0.2 percentage points.

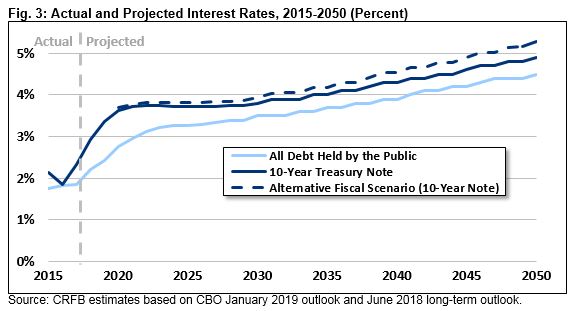

Indeed, CBO projects interest rates on ten-year Treasury notes will rise from 2.9 percent in 2018 to 3.8 percent by the end of the decade and 4.8 percent by 2048. Under the Alternative Fiscal Scenario where debt rises even higher, interest rates would likely exceed 5.1 percent by 2048.

At some point, rising debt could increase interest rates much more significantly. The figures above assume rates rise due to increased demand for debt financing. If debt grew to the point that markets believed there was a risk that the federal government would accommodate inflation or other means of implicit or explicit default, interest rates could rise to much higher levels.

Rising Debt Reduces Fiscal Space to Combat the Next Crisis

During economic recessions, as well as wars and other emergencies, it may be necessary or even desirable to run large deficits. Yet the higher deficits and debt are in advance of a recession or crisis, the less “fiscal space” a country will have to finance or combat that crisis.

A recent study by Christina Romer and David Romer found that countries that enter crises with high levels of debt tend to do less to combat the crisis and thus recover more slowly. Romer and Romer find that both economic and political constraints to borrowing are higher when debt is high; they recommend countries reduce their debt during good times to create more fiscal space.

When the United States entered the Great Recession, for example, the country’s debt-to-GDP ratio stood at 35 percent – roughly its historical average. By 2012, the country had borrowed an additional 35 percent of GDP, largely to combat the crisis. Under our current trajectory, it is not clear the United States would have the fiscal space to repeat this magnitude of intervention.

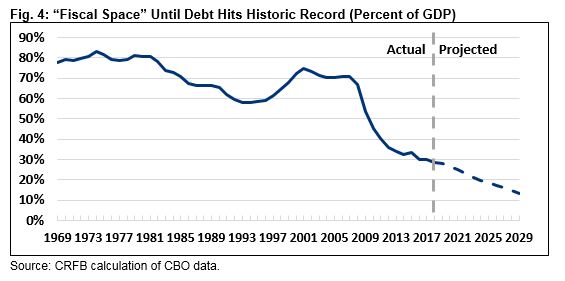

While there’s no way of knowing how much fiscal space the United States has, one illustrative measure could focus on the room before reaching the all-time record debt level of 106 percent of GDP set in 1946. While it is unlikely this represents an economic constraint on borrowing, it does represent when the debt level would be unprecedented and may serve as a political constraint.

Under this illustrative measure, the United States has 28 percent of GDP in fiscal space today, declining to only 13 percent by 2029 under current law. Under current policy, fiscal space until debt hits record levels would virtually disappear by the end of the decade. This deteriorating fiscal space suggests it will become increasingly difficult to effectively respond to future crises.

Importantly, less fiscal space could also make it harder for the country to address new challenges and opportunities. Updating the country’s social contract, establishing a Green New Deal, or ending impediments to capital growth is extremely hard when debt is so high and potential financing sources are already needed to keep the existing fiscal situation under control.

Rising Debt Places an Increased Burden on Future Generations

The national debt is fundamentally a generational issue. Continued borrowing to finance tax cuts or spending for consumption today creates an increased burden on young and future Americans.

A child born in the United States today will immediately inherit almost $50,000 of national debt. While that debt will never need to literally be paid back, it nonetheless has costs.

For one, the economic consequences of debt will be felt most heavily by younger and future generations. Slowing income, rising interest rates, and declining fiscal space all cumulate over time. CBO estimates rising debt will reduce GNP by 1 percent after ten years, 2 percent after 20 years, and 6 percent after 30 years, when compared to falling debt.

In addition, the unsustainable path of the debt means that low taxes or high spending today will ultimately need to be offset, to some degree, by the future. By borrowing more today, policymakers are all but assuring higher taxes and lower spending on future taxpayers and government beneficiaries. At a minimum, younger and future generations will face an increasing interest burden, and debt service will continue to climb.

Indeed, rising interest costs may already be adversely affecting future generations. By next year, the federal government is projected to spend more on servicing its debt obligations than it does on all programs and funding for children. In other words, the government will spend more on funding the last generation’s consumption than investing in the future.

With so many unmet needs already and new challenges and opportunities emerging, the United States does not need to spend the rest of the 21st century focused on paying for the past.

Rising Debt Increases the Risk of a Fiscal Crisis

The United States is unlikely to face a fiscal crisis anytime soon, but if debt continues to rise and it becomes increasingly clear that trend will not reverse, the risk of a crisis will grow.

The fact that the United States borrows in its own currency makes default or insolvency highly unlikely. The country’s strong economy, steady monetary policy, stable political system, and full faith and credit in paying our sovereign debt has so far stemmed any worries that the U.S. wouldn’t fulfill its obligations. But this may not last forever. Endless deficit spending, tax cuts, and refusal to make the tough choices of what to prioritize will eventually lead investors to question our creditworthiness.

A fiscal crisis could take many forms. In a 2010 paper on the topic, CBO describes the possibility of a debt-fueled financial crisis. In this scenario, high and rising debt could result in a market panic that leads investors to demand higher interest rates. This spike in rates, in turn, would erode the value of the U.S. debt held around the world (currently about $14 trillion), triggering a selloff of federal bonds. Given the structural role those safe assets play in the financial system, the result could be a global financial crisis.

Alternatively, a fiscal crisis could take the form of rapid inflation. If borrowing were sufficiently high or demand for U.S. debt sufficiently low, the federal government could find itself printing new money in order to pay its debt. While countries can often engage in modest monetary expansion or seigniorage without disruption, continuously expanding the money supply to chase ever-rising deficits is a recipe for hyperinflation. The implementation of new heterodox economic practices designed to facilitate such printing could itself spark this inflation by undermining price stability.

High debt could also force the country to engage in austerity during an economic recession in order to avoid one of the above scenarios. This austerity itself could create a crisis by expanding unemployment and holding the economy well below potential for an extended period of time.

Importantly, while high and rising debt increases the likelihood of a fiscal crisis, it is impossible to predict what might spark such a crisis. One possibility is a change in the attitudes of foreign creditors, who for economic or geopolitical reasons may choose to sharply adjust their debt holdings. A recession or financial crisis could also bleed into a fiscal crisis, as has been the case with numerous fiscal crises through history. A fiscal crisis could also emerge from a market panic over the sustainability of U.S. fiscal policy and reliability of the country’s institutions, which could be undermined by the adoption of new fringe economic theories that put monetary policy in the hands of elected officials.

Luckily, the risk of a fiscal crisis in the United States remains low. But there is no guarantee it will remain that way. The higher and faster debt rises, the greater the likelihood a crisis will occur.

Conclusion

The U.S. government is deeply in debt. While measuring the country’s fiscal position in trillions of dollars or percentage points of GDP may seem abstract, the adverse consequences of continuing on our current trajectory are real.

In this paper, we discuss some of these consequences – rising debt slows income growth, increases federal interest payments, pushes up interest rates, reduces our ability to respond to the next recession or emergency, burdens younger and future generations, and increases the risk of fiscal crisis.

As an addendum to this paper, we have also drafted a debt Question & Answer piece responding to some of the claims that suggest debt does not matter.

In future papers, we will discuss other negative consequences of high and rising debt – including how it can damage thoughtful policymaking, weaken political institutions, and hurt the country’s geopolitical standing. Former Chairman of the Joint Chiefs of Staff Admiral Mike Mullen has repeatedly declared “the most significant threat to our national security is our debt.”

Rather than putting our national and economic security further at risk and enhancing the negative consequences of borrowing by adding more to the debt, policymakers should pay for new proposals and come together on policies to improve our fiscal situation. Without a solution, the consequences of debt will gradually worsen over time and may be difficult to reverse.

For more information, read Why Should We Care About the National Debt: Questions and Answers.