Analysis of the President’s FY 2020 Budget

The Trump Administration released its Fiscal Year (FY) 2020 budget proposal today, outlining the President’s tax and spending priorities over the next decade. By the budget’s own estimates, it would put debt on a downward path relative to the economy after 2022 and balance the budget within 15 years.

We support the President’s goal of reducing debt relative to GDP and are pleased he offers a reasonable timeframe for eventual balance. We also welcome the budget’s thoughtful proposals to slow health care cost growth and reform various spending programs.

However, the budget is riddled with gimmicks and unrealistic assumptions. In particular, it hides the cost of extending tax cuts in its baseline, circumvents budget caps in order to extend recent defense hikes through a war spending account, and relies on incredibly rosy economic growth assumptions.

In this paper, we analyze the budget. Our main findings include:

- According to the Office of Management and Budget (OMB), debt under the President’s budget would fall from 78 percent of Gross Domestic Product (GDP) today to 71 percent of GDP by 2029. Using more realistic assumptions on economic growth, we estimate debt would rise to roughly 87 percent of GDP.

- The budget claims $2.8 trillion of net deficit reduction over a decade. However, incorporating the $1.1 trillion cost of extending tax cuts and excluding assumed reductions in war spending, actual savings in the budget would total $1.2 trillion.

- Discretionary proposals in the budget are both misleading and unrealistic. The President proposed $1 trillion of defense hikes, using a special war spending designation to circumvent spending caps in 2020 and 2021. The budget also calls for $1.1 trillion of largely unspecified non-defense cuts, reducing spending to about 60 percent of today’s (inflation-adjusted) levels by 2029.

- The President’s budget puts forward a number of thoughtful mandatory spending changes (and a few proposals to increase receipts) – especially reforms to Medicare which would reduce costs of beneficiaries and taxpayers.

- Projections in the President’s budget are heavily influenced by extremely rosy economic assumptions. OMB assumes average real GDP growth of nearly 3 percent per year, while most forecasters project less than 2 percent annual growth.

While we are encouraged that the President’s budget includes a reasonable fiscal goal and thoughtful deficit reduction policies, in reality the budget would fail to meet even the goal of stabilizing the debt. The budget relies far too heavily on unrealistic assumptions, back-door tax cuts, and defense spending increases.

Spending, Revenue, Deficits, and Debt in the President’s Budget

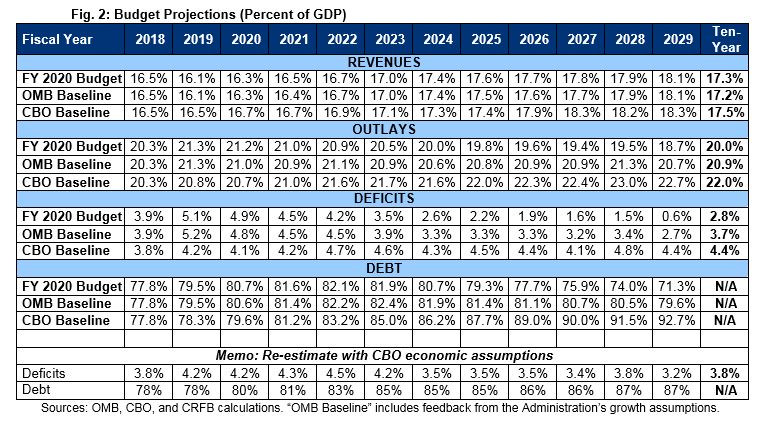

According to its own estimates, the President’s budget would substantially slow the growth of debt – though the Administration’s rosy economic assumptions already suggest roughly stable debt levels absent the budget. Specifically, debt would grow from $16.2 trillion today to $24.8 trillion by 2029 under the President’s budget, compared to $27.6 trillion under OMB’s baseline.

As a share of GDP, under the President’s budget, debt would increase from 78 percent in 2018 to 82 percent in 2022 before declining to 71 percent of GDP by 2029. By comparison, debt under OMB’s baseline will remain relatively stable and total nearly 80 percent by 2029.

Removing OMB’s rosy economic assumptions, the Congressional Budget Office’s (CBO) baseline estimates debt will reach 93 percent of GDP by 2029. Based on those same assumptions, we estimate debt under the President’s budget would rise to roughly 87 percent of GDP by 2029.

Under the President’s budget projections, annual deficits would increase in the near term but fall over the rest of the decade. Specifically, the deficit would increase from $779 billion in 2018 to $1.1 trillion in 2020 before falling to $202 billion in 2029. As a share of GDP, deficits would increase from 3.8 percent in 2018 to 5.1 percent in 2019 before falling to 0.6 percent by 2029. By comparison, OMB’s baseline projects a deficit of 2.7 percent of GDP ($927 billion) in 2029. Again, realistic economic assumptions would result in higher deficits both under the baseline and under the President’s budget. Using CBO economic assumptions, we estimate the deficit in 2029 would still be more than 3 percent of GDP.

Based on the budget’s numbers, revenue would fall as a share of GDP in the near term but ultimately grow to exceed its historical average, while spending as a share of GDP would fall over time. Specifically, spending would fall from 20.3 percent of GDP in 2018 to 18.7 percent by 2029, while revenue would shrink from 16.5 percent of GDP in 2018 to 16.1 percent by 2019 before growing to 18.1 percent by 2029. By contrast, revenue and spending in the OMB baseline would total 18.1 percent and 20.7 percent, respectively, in 2029.

Spending decreases relative to GDP are largely driven by assumptions of a rapidly growing economy as well as cuts to non-defense discretionary programs. Reductions in the growth of Medicaid, Medicare, welfare-related programs, and other mandatory programs also help spending levels to decline relative to GDP.

The near-term decline in revenue under the budget is driven by tax cuts in effect as a result of the 2017 tax law. Assumptions of rapid economic growth, along with certain elements of the tax cuts that raise more or lose less over time, largely explain the growth in revenue over the next decade.

Proposals in the President’s Budget

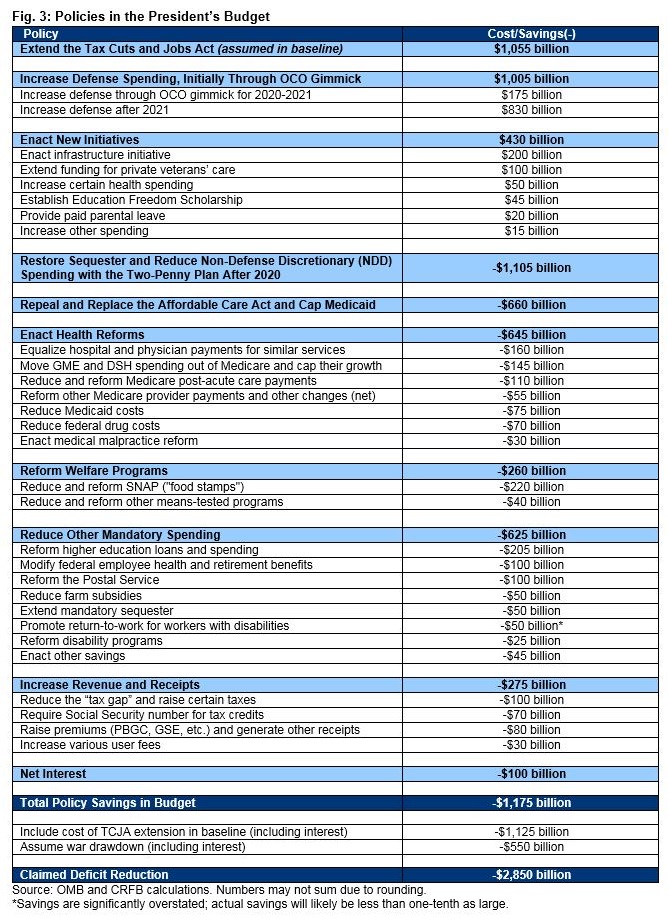

The President’s budget estimates it would achieve about $2.8 trillion in deficit reduction over a decade. However, these estimates do not include the costs of extending parts of the 2017 tax law (embedded in OMB’s baseline), and counts a near zeroing out of war funding in future years as a budgetary savings.

Adjusting for these assumptions results in $1.2 trillion in net deficit reduction from policies, including $1.1 trillion in reductions to non-defense discretionary spending, $1.3 trillion in health savings, $1.2 trillion in other deficit reduction, and $100 billion of interest savings – partially offset by $430 billion of spending and tax breaks for new initiatives, $1 trillion in defense increases, and $1.1 trillion of tax cuts embedded in the baseline.

Extend the Tax Cuts and Jobs Act ($1.1 trillion) – The President’s budget assumes that tax provisions for individuals that are otherwise set to expire after 2025 under the 2017 tax law would instead be extended. Because this assumption is built into the President’s baseline, it does not appear as a new initiative in the budget itself. However, it would substantially increase deficits relative to current law or what was projected after the tax law’s passage.

Increase Defense Spending, Initially Through the OCO Gimmick ($1 trillion) – Under current law, defense spending is scheduled to fall by 11 percent next year as recent spending increases are replaced with sequester-level caps. The President’s budget calls for avoiding these cuts and instead increasing defense spending by 5 percent this year and additional amounts over the next decade. To avoid raising the 2020 discretionary cap on defense spending, the budget funds this year’s defense increase through the Overseas Contingency Operations (OCO) account, which is designated for war spending and not subject to the caps. This blatant gimmick is repeated for 2021, after which the Administration proposes to fund nearly all defense spending through the ordinary budget category.

Enact New Initiatives ($430 billion) – The President’s budget proposes roughly $430 billion of spending and tax breaks on new initiatives. Most significantly, the budget includes a $200 billion infrastructure proposal. The budget also proposes to spend $20 billion of spending and tax breaks to provide for paid parental leave, $45 billion for a new school choice scholarship program, $40 billion to allow more health insurance plans to offer Health Savings Accounts, and $100 billion to fully fund the VA MISSION Act of 2018 outside of the discretionary budget.

Restore Sequester and Reduce Non-Defense Discretionary (NDD) Spending with the Two-Penny Plan After 2020 (-$1.1 trillion) – The President’s budget would allow non-defense discretionary spending to return to the sequester level in 2020, a 9 percent reduction from 2019 levels. Beyond that, the Administration calls for a further 2 percent per year reduction (the “two-penny plan”), even as inflation rises by a similar amount. These cuts would result in total NDD appropriation reductions of $1.1 trillion over ten years and a $235 billion cut in 2029 – about 30 percent below baseline and about 40 percent below 2019 inflation-adjusted levels.

Repeal and Replace the Affordable Care Act and Cap Medicaid (-$660 billion) – The President’s budget proposes to repeal and replace the Affordable Care Act (ACA or “Obamacare”) in a similar manner as the Graham-Cassidy-Heller-Johnson proposal. This would replace the ACA’s premium subsidies and Medicaid expansion with either a flexible state block grant or per-capita cap while also capping the growth of base Medicaid. Growth of both the block grant/cap and Medicaid would be limited to inflation. The Administration estimates this would save $660 billion over a decade after program interactions.

Enact Health Reforms (-$645 billion) – The budget also proposes $645 billion in health care savings largely from reforming and reducing Medicare provider payments. Specifically, the budget would equalize payments for similar services offered in hospitals and physician’s offices, slow the growth of post-acute care payments, and reduce compensation to hospitals for bad debts. In addition, the President’s budget proposes to remove payments for medical residents (graduate medical education) and uncompensated care (disproportionate share hospital payments) out of Medicare and into their own programs while capping their growth. (Note this proposal has led some to wrongly assume nearly $850 billion of Medicare cuts in the budget by counting as savings spending that would be moved from Medicare to another program). The President’s budget also proposes a number of policies designed to reduce spending on prescription drugs by about $70 billon. In addition, the budget includes about $75 billion of assorted Medicaid savings (outside of caps and ACA changes) and estimates about $30 billion of savings from enacting medical malpractice reform. Importantly, these changes would significantly reduce health care spending both for the federal government and for Medicare beneficiaries.

Reform Welfare Programs (-$260 billion) – The President’s budget would pare back and reform several safety net programs. It would reduce the Supplemental Nutrition Assistance Program (SNAP or "food stamps") by $220 billion through home-delivered food boxes, eligibility limitations, and program integrity improvements. The budget would save another $40 billion through other means-tested programs, including by eliminating Social Services Block Grants and cutting the size of Temporary Assistance for Needy Families (TANF) block grants.

Reduce Other Mandatory Spending (-$625 billion) – The President’s budget includes a variety of other cuts and changes to other mandatory spending. As with last year’s budget, it includes more than $200 billion of savings on higher education by consolidating the multiple income-driven loan repayment programs into a single plan with a higher cap on monthly repayments, eliminating the in-school interest subsidy, and ending public service loan forgiveness. The budget also saves around $100 billion from modifying federal employee health and retirement benefits, $100 billion from reforming the postal service, $50 billion from reducing farm subsidies, and $45 billion from other savings. In addition, the budget proposes thoughtful reforms to the Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) disability programs; of the $75 billion in claimed savings, two-thirds come from optimistic assumptions of the effectiveness of return-to-work programs while the other third comes from measurable savings.

Increase Revenue and Receipts (-$275 billion) – Additional deficit reduction in the budget comes from increases to government receipts and, in some cases, increases in tax revenue. For example, the budget would increase tax revenue by $45 billion from funding the IRS to conduct audits, and by another $100 billion from requiring Social Security numbers in order to collect tax credits, requiring states to raise their unemployment taxes to finance paid family leave, and ending several tax breaks for renewable energy. The budget also generates nearly $30 billion from new user fees on immigration, customs, and food inspection, among other things. It also raises premiums related to the Pension Benefit Guaranty Corporation and Government-Sponsored Enterprises like Fannie Mae and Freddie Mac. Finally, the budget also generates additional funds by selling or leasing various government assets, including wireless spectrum.

Economic Assumptions

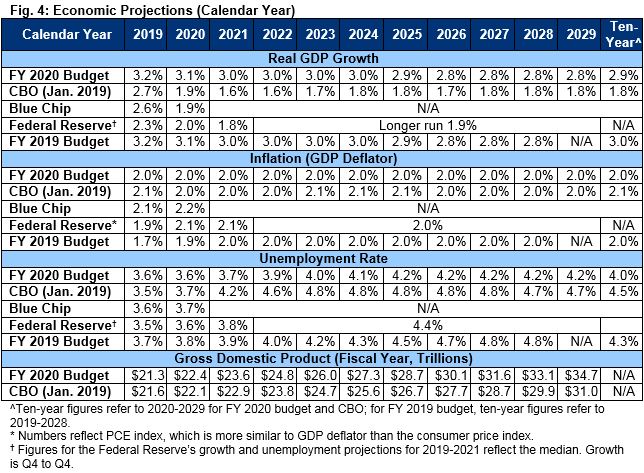

A budget’s economic assumptions underlie every single estimate it makes. The assumptions in this President’s budget – as in the past two budgets – are overly optimistic and far outside of mainstream forecasts. While it is certainly reasonable that a budget assumes its policies have an effect on the economy, this budget’s growth assumptions, which average nearly 3 percent over a decade, are unlikely to reflect reality.

OMB projects real (inflation adjusted) GDP growth of 3.2 percent in 2019 and 3.1 percent growth for 2020, eventually tapering down to 2.8 percent in 2026 and beyond.

The economic projections in this budget are much more optimistic than other forecasters, especially over the medium and long term. Despite decade-high 2.9 percent growth in 2018, much of that growth will likely prove to be temporary due to the stimulative effects of recent tax cuts and spending increases. Absent this stimulus, the aging population suggests growth rates will be closer to, and possibly below, 2 percent per year.

CBO, for example, expects growth to fall to 2.7 percent in 2019 and 1.9 percent in 2020 before leveling off around 1.7 to 1.8 percent for the rest of the decade. Likewise, the Federal Reserve projects long-term sustained growth of 1.9 percent per year, and the Blue Chip average for sustained growth is only slightly higher.

Over time, OMB’s rosy growth assumptions lead them to project a much larger economy than others do. For example, OMB estimates GDP would total nearly $35 trillion in 2029 – a full 12 percent above CBO’s $31 trillion projection.

These differences allow OMB to assume much smaller levels of debt. If we used CBO’s economic assumptions instead, we estimate (very roughly) that debt would reach 87 percent of GDP by 2029, rather than falling to 71 percent.1

OMB’s excess GDP assumptions are especially curious given that their interest rate assumptions are similar to other estimates. Typically, a percent of faster growth would lead to about a percent increase in interest rates – thus neutralizing some of the fiscal feedback from faster growth (since it would mean higher interest payments). Yet OMB projects about a percentage point more of growth than CBO, despite estimating that three-month and ten-year Treasuries would settle at 3.0 percent and 3.7 percent, respectively – in line with CBO’s estimates of 2.8 and 3.7 percent.

The other economic indicators in the President’s budget are also roughly in line with other forecasts. OMB projects the unemployment rate to average 3.6 percent in 2020, which is the same as the Federal Reserve’s estimate. And it expects the unemployment rate to increase to 4.2 percent in 2025 and remain there through 2029, which may be a little optimistic but is still in line with other forecasts.

OMB projects inflation as measured by the GDP deflator to remain basically flat at 2 percent, similar to projections made by other forecasters.

Conclusion

We are encouraged that the President’s budget sets a reasonable fiscal goal that, according to its estimates, would put debt on a downward path relative to the economy. The President’s budget deserves praise for putting forward a number of thoughtful policies to reduce spending growth. The Medicare policies in the President’s budget, in particular, would reduce costs and improve value of care for beneficiaries while also slowing the growth of the second largest and fastest growing program in the budget.

Unfortunately, the budget relies on a series of gimmicks to cut taxes and increase defense spending by over $1 trillion each – the former by hiding the cost in the baseline and the latter by abusing the OCO designation meant to cover war spending. These gimmicks not only produce bad fiscal outcomes but also perpetuate bad budget processes.

Equally troubling, the budget relies on extremely rosy economic growth projections to mask large deficits. Using more realistic growth assumptions, debt would rise to roughly 87 percent of GDP rather than falling to 71 percent.

Substantial new revenue and spending cuts are still needed to address our rising debt, even if the President’s budget were enacted in its entirety.

With recent discretionary spending cap increases slated to expire and as the debt ceiling returns, we worry the pressure will be for more deficits, not less.

The Administration has an opportunity to lead on fiscal issues this year to assure that cap increases are offset and deficit reduction is considered.

But leadership means putting all parts of the budget and tax code on the table to find savings and new revenue, not papering over the problem with gimmicks, gains, and fantasy growth.

1 This is a rough initial estimate subject to revision.

What's Next

-

Image

-

-