How Much Does the House GOP Tax Plan Cost?

The tax reform conversation so far has mostly focused on House Republicans' "Better Way" Blueprint released last summer (we explain the plan in detail here). One of the most important questions in evaluating this plan will be understanding its fiscal effect. Unfortunately, too little information exists to provide a definitive cost estimate at this time, but we do have some clues. Based on available estimates, more work needs to be done to ensure tax reform helps rather than damages our overall fiscal situation.

In this piece, we show that:

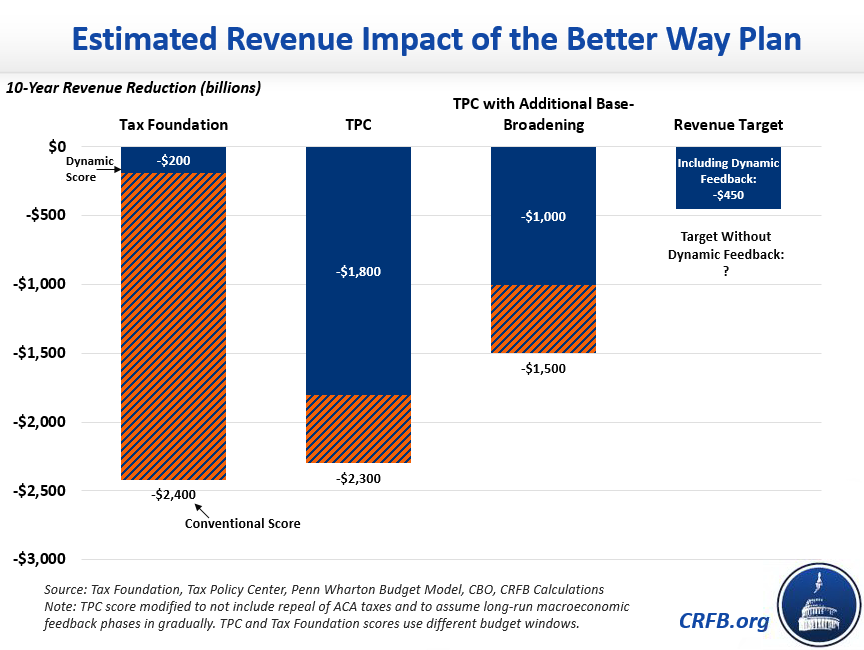

- The Better Way Blueprint's "current policy" revenue target suggest their plan will cost at least $450 billion over a decade under dynamic scoring (including economic growth effects).

- The provisions specified in the Blueprint would cost $2.3 trillion over a decade, based on conventional estimates by the Tax Policy Center (TPC).

- The Tax Foundation estimates these same policies would cost $2.4 trillion over a decade.

- The Blueprint implies policy changes beyond those it specifically mentions. Assuming it also eliminates all "special interest" tax breaks, its conventional cost would fall to $1.5 trillion.

- The Blueprint is likely to promote economic growth, which based on TPC's estimates we project would generate about half a trillion dollars of revenue. Under dynamic scoring, the provisions detailed in the Blueprint would therefore cost $1.8 trillion, and with the elimination of special interest tax breaks would cost about $1.0 trillion.

- Tax Foundation projects much stronger economic growth, and therefore estimates a dynamic cost of only $200 billion.

- Most of the Blueprint's costs are transitional. In the second decade, we estimate the plan's provisions would cost only $800 billion and in the best case scenario the plan could actually raise as much as $1.55 trillion.

Cost Break-Down of the Better Way Tax Plan

The "Better Way" Blueprint is an outline, not a fully-detailed proposal or piece of legislation. But it does propose a revenue target – revenue-neutrality on a dynamic basis relative to "current policy." Because it defines "current policy" to include the extension of many tax provisions scheduled to expire, this revenue target suggests their plan would cost about $450 billion under dynamic scoring (which incorporates economic growth effects), and likely more under conventional scoring.

So far, the details provided by the Better Way Blueprint would fall significantly short of this target. Two organizations have estimated the cost the specified provisions of the plan in its entirety – the Tax Policy Center (TPC) and the Tax Foundation (TF). Based on TPC's estimates of the tax reform plan only (excluding the tax provisions of the health care reform plan), the provisions of the Better Way plan explicitly mentioned in the Blueprint would cost $2.3 trillion over the next decade under conventional scoring. Equivalent estimates from TF are close at $2.4 trillion (though they use a different 10-year window).

Both organizations estimate that the majority of the revenue loss in the first decade is due to business tax changes. TPC finds that lowering the corporate rate to 20 percent would cost about $1.85 trillion (TF estimates $1.8 trillion) over a decade, reducing the top rate on pass-through business income to 25 percent would cost $400 billion (TF estimate = $500 billion), and allowing full expensing in exchange for eliminating interest deductibility would cost $1.1 trillion (TF estimate = $1.05 trillion). These costs would be paid for in part by making the business tax border adjustable, raising $1.2 trillion (TF estimate = $1.05 trillion) over a decade, and a variety of other business tax changes that would raise a combined $200 billion, on net (TF estimate = $750 billion).

On the individual side, rate reductions would lose $1.55 trillion (TF estimate = $1.95 trillion), replacing preferential rates with a 50 percent exclusion for capital income will cost $500 billion (TF estimate = $600 billion), eliminating the AMT would cost $450 billion (TF estimate = $350 billion), and repealing the estate tax would cost $350 billion (TF estimate = $250 billion). Meanwhile, replacing personal exemptions with an enhanced standard deduction and child and dependent tax credits would result in a net loss of about $50 billion (TF estimate = $150 billion). Part of these costs would be offset by repealing most itemized deductions, raising $1.9 trillion (TF estimate = $2.35 trillion), and ending a variety of other individual tax breaks, raising $400 billion (TF estimate = $100 billion).

Tax Policy Center and Tax Foundation Scores of the Better Way Plan (Billions)

| Provision | TPC | TF |

|---|---|---|

| Eliminate the Alternative Minimum Tax | -$450 | -$350 |

| Reduce rates to 12, 25, and 33 percent | -$1,550 | -$1,950 |

| Repeal itemized deductions (other than charitable and mortgage interest) and Pease | $1,900 | $2,350 |

| Replace personal exemptions with increased standard deduction and child & dependent tax credits | -$50 | -$150 |

| Create 50 percent exclusion for capital income | -$500 | -$600 |

| Repeal select other individual tax preferences | $400 | $100 |

| Repeal the estate tax | -$200 | -$250 |

| Individual and Estate Tax Reform | -$350 | -$850 |

| Reduce corporate income tax rate to 20% and repeal corporate AMT | -$1,850 | -$1,800 |

| Tax income from pass-through businesses at a top rate of 25% | -$400 | -$500 |

| Adopt full expensing of new purchases; disallow interest deduction on new loans | -$1,100 | -$1,050 |

| Apply a border adjustment to the business tax | $1,200 | $1,050 |

| Enact other international tax reforms | $50 | $50 |

| Repeal select other corporate tax expenditures | $150 | $700 |

| Business Tax Reform | -$1,950 | -$1,550 |

| Cost of Specified Tax Reform (Conventional) | -$2,300 | -$2,400 |

| Dynamic Feedback | $500* | $2,200 |

| Cost of Specified Tax Reform (Dynamic) | -$1,800 | -$200 |

| "Special Interest" tax breaks not addressed in the Blueprint | $800 | N/A |

| Cost assuming repeal of all “special interest” tax breaks (Conventional) | -$1,500 | N/A |

| Dynamic Feedback | $500* | N/A |

| Cost assuming repeal of all "special interest" tax breaks (Dynamic) | -$1,000 | N/A |

| House GOP Revenue Target (Dynamic) | -$450 | -$450 |

Source: Tax Foundation, Tax Policy Center, and CRFB calculations.

*TPC dynamic feedback estimated based on TPC and PWBM estimates of short- and long-run macroeconomic effects and CRFB calculations. TPC and Tax Foundation scores use different budget windows.

Numbers may not sum due to rounding.

Additional Provisions and Feedback Effects Could Change the Score

Importantly, the estimates described above are based only on what is explicitly outlined in the Better Way Blueprint. The Blueprint also calls for vague reforms to the mortgage interest and charitable deductions and for eliminating "special interest" tax breaks. Legislative language is also likely to adopt other tax reform changes to help pay for the plan.

To get a sense of the magnitude of possible savings, TPC identifies what they consider to be "special interest" tax breaks. Repealing them would raise an additional $800 billion over the 10-year budget window, which would reduce the ten year cost from $2.3 trillion to $1.5 trillion. Additional changes could further reduce the cost.

Tax reform structured like the Better Way is likely to increase economic growth. To the extent it does, the bill could also generate additional "dynamic gains." Based on TPC's estimate of the near- and long-term economic effects, we estimate potential dynamic gains of up to $500 billion over 10 years. That would lead to a total cost of $1.8 trillion from specified provisions and about $1.0 trillion if all "special interest" tax breaks were eliminated. From there, one could envision sufficient additional changes to reduce the total cost to the stated revenue target of $450 billion in revenue reductions.

Interestingly, the Tax Foundation estimates far larger economic gains than does TPC. Based on TPC's estimates, the plan would increase the size of the economy by about 1 percent after a decade; Tax Foundation estimates the economy could be 9 percent higher. As a result, they estimates dynamic feedback of $2.2 trillion and therefore a total cost of only $200 billion. It is important to note, however, that Tax Foundation's model appears to differ significantly from the models used by official scorekeepers like CBO and JCT, in part because it does not account for the economic cost of high debt.

The Long-Run Cost of the Better Way Tax Plan

While the upfront costs of the components of the Better Way blueprint are quite expensive, many of these costs are transitional and will fall over time. Specifically, the switch to full expensing of capital investment in place of gradual depreciation results in very high one-time costs followed by significantly lower permanent costs. Meanwhile, eliminating the deductibility of interest on new loans will raise very little in the near-term but generate very large amounts of revenue over the long-term.

TPC estimates these two changes would lose about $1.1 trillion on net in the first decade but actually raise $1.1 trillion in the second decade. As a result, TPC estimates suggest the full tax plan would reduce revenues by $800 billion in the second decade (as compared to $2.3 trillion in the first). The Tax Foundation also estimates the cost of the plan will fall over time, with the conventional revenue loss falling from 1.1 percent of GDP in the first decade to 0.5 percent in the second (roughly $1.7 trillion), and eventually declining to 0.4 percent of GDP. With dynamic scoring, we estimate very little long-term dynamic revenue loss. And with the elimination of "special interest tax breaks," the plan could generate up to $550 billion in revenue gains in the second decade, or over $1.5 trillion on a dynamic basis.

Importantly, our long-run estimates assume the border adjustment continues to raise significant revenue over the long-run. It will not raise as much if trade deficits shrink dramatically or even turn to trade surpluses over time.

Revenue Impact of the Better Way Tax Plan Provisions (Billions)

| Provision | 1st Decade | 2nd Decade |

|---|---|---|

| Repeal the Alternative Minimum Tax | -$450 | -$700 |

| Reduce rates to 12, 25, and 33 percent | -$1,550 | -$2,600 |

| Repeal itemized deductions (other than charitable and mortgage interest) and Pease | $1,900 | $3,350 |

| Replace personal exemptions with increased standard deduction and child & dependent tax credits | -$50 | $200 |

| Create 50 percent exclusion rate for capital income | -$500 | -$850 |

| Repeal select other individual tax preferences | $400 | $550 |

| Repeal the estate tax | -$200 | -$300 |

| Individual and Estate Tax Reform | -$350 | -$400 |

| Reduce corporate income tax rate to 20% and repeal the corporate AMT | -$1,850 | -$2,750 |

| Tax income from pass-through businesses at a top rate of 25% | -$400 | -$700 |

| Adopt full expensing of new purchases; disallow interest deduction on new loans | -$1,100 | $1,100 |

| Apply a border adjustment to the business tax | $1,200 | $1,700 |

| Enact other international tax reforms | $50 | -$150 |

| Repeal select other corporate tax expenditures | $150 | $350 |

| Business Tax Reform | -$1,950 | -$400 |

| Cost of Specified Tax Reform (Conventional) | -$2,300 | -$800 |

| Dynamic Feedback* | $500 | $750 |

| Cost of Specified Tax Reform (Dynamic) | -$1,800 | -$50 |

| “Special Interest” tax breaks not addressed in the Blueprint | $800 | $1,350 |

| Cost assuming repeal of all “special interest” tax breaks (Conventional) | -$1,500 | $550 |

| Dynamic Feedback* | $500 | $1,000 |

| Cost assuming repeal of all "special interest" tax breaks (Dynamic) | -$1,000 | $1,550 |

| House GOP Revenue Target (Dynamic) | -$450 | N/A |

Source: Tax Policy Center, Penn Wharton Budget Model, Congressional Budget Office, CRFB calculations.

*Dynamic feedback estimated based on TPC and PWBM estimates of short- and long-run macroeconomic effects and CRFB calculations.

Numbers may not sum due to rounding.

The long-term revenue gain would still fall far short of the first-decade revenue loss – unless all special interest tax breaks were repealed and dynamic scoring was incorporated – even before considering the cost of additional interest on the debt. Lawmakers should ensure tax reform is revenue-neutral in the first decade, and dedicate dynamic gains from economic growth and an expanding long-term revenue base toward deficit reduction. Still, the fact long-term cost estimates are so much smaller than near-term estimates suggests that thoughtful transition rules can help close the ten-year revenue gap.

Conclusion

The House GOP "Better Way" tax plan represents a thoughtful overhaul of the tax code that could help to promote economic growth and achieve a variety of other important gains. But the revenue target proposed within the plan is insufficient, and the details put forward so far fall well short of even that target. Tax reform should help improve, not worsen, our fiscal situation, and should at the very least raise as much revenue as the current tax code. House Republicans can make their plan more fiscally responsible by including additional base-broadening measures, phasing in changes over time, or not cutting tax rates so aggressively. Tax reform offers an opportunity to move the tax code in a simpler and more pro-growth direction, but any changes need to be paid for.

Read More About Current Tax Reform Efforts:

- Five Reasons to Pay for Tax Reform

- Lowering the Bar for "Revenue Neutral" Tax Reform

- House GOP Sketches Out Details on Tax Reform

Update (4/17/2017): Dynamic estimates are based off of TPC's orginal analysis of the Better Way plan. For their more recent analysis, see here.