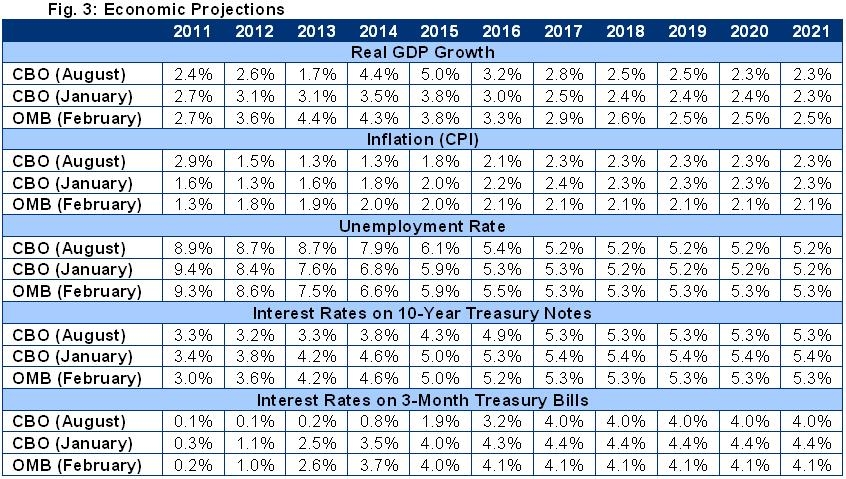

CBO's Newest Economic Projections

In CBO's latest Budget and Economic Outlook, CBO includes revised projections of various economic indicators as part of its update. Since there is such a major relationship between economic conditions and fiscal policy, these numbers are of significant importance. CBO's latest economic projections do contain worse real GDP growth for the first few years, but much faster growth mid-decade. However, CBO notes in its update, that "[t]incorporating that recent news and economic data would have led CBO to temper its near-term forecast for economic growth". CBO notes that these projections were done in early July and did not have time to re-do them to incorporate some of the significant economic news which points to even slower growth than originally projected.

For example, today's Bureau of Economic Analysis release of dismal revised second quarter real GDP numbers with the annual growth rate for the second quarter equal to 1.0 percent. With economic projections such as that, coming after early July, it is likely, as CBO explains, that their own economic outlook, at least in the short term, would likely have been changed due to recent events, which of course would also change their fiscal outlook.

Some other reasons for pessimism from CBO include:

- 15 percent drop between early July and mid-August in the S&P 500 stock index

- BEA revision of GDP from 1.9 to 0.8 for the first half of the year

- Downward revision of the recession from -4.1% to -5.1% from fourth quarter 2007 to second quarter 2009

In addition to changes in growth estimates, CBO is now estimating interest rates will be far lower in both the near- and long-term. In the short-run, the lower rates are based largely on observation -- and are likely a result of a weaker economy as well as decisions by the Federal Reserve to maintain a low federal funds rate. Over the long-term, the lower interest rates come mainly as a result of the marked improvement in the fiscal picture (though this improvement is based largely on an unrealistic baseline and on the assumption the Super Committee identifies $1.2 trillion in yet-unspecified savings). With debt declining as a share of GDP, CBO estimates interest rates will remain lower than they otherwise would be.

As a result of these factors, CBO projections more than $630 billion less in net interest spending than they did in March. This savings might not materialize, if the United States fails to get its fiscal house in order.